Insights from Modern Principles of Economics

How good are our economists? Look around. On a 20-minute walk to my Berkeley office, I walked past people reeking of urine, past people lying in a dirty sleeping bag on a thin cardboard pad, past some garbage around a tent which housed a child who grew up into an impoverished adult.

In what world is this broader system a success story for economics?

In this world.

Economics is important.

The availability heuristic can deceive you (although Kaj Sotala notes that e.g. the Bay area homeless may be benefitting less from growth than the global poor). If you just look out your window, you might miss important global trends.

Good economic policy has lifted billions of people out of poverty and furnished our lives with previously unimaginable splendor. The Roman emperors had no air conditioning or telephones.

Economists are not responsible for all of this growth. I wasn’t able to quickly find counterfactual estimates for the importance of economic theories, but my impression is that several advances in economics have in fact significantly improved economic policy.

Good economic policy is a weapon against suffering, against disease and disorder and squalor, and perhaps one day against death itself.

Good economic policy makes selfish actors conspire to deliver cheap, delicious pastries to your doorstep in less than an hour.

Good economic policy is often about expanding the pie, instead of fighting over who gets what part today. This very moment, a vast universe full of energy and resources burns away.

Before reading this book, I tried some other econ textbooks. They were bad. Before the bad textbooks, economic analysis had seemed like “just another consideration.” I’d taken an econ class in college, and kiiiinda remembered what “deadweight loss” meant.

When I read Cowen and Tabarrok’s Modern Principles of Economics, I regularly felt beliefs getting debunked and replaced with less wrong beliefs—an experience last felt while reading the sequences.

As a teenager, I thought that:

stimulus = good because obviously people need money in a recession, and they’ll spend that money

tax cuts = bad because they won’t be spent as much, and usually tax cuts are just excuses to reduce tax burden on the rich

outgroup members thought homeless people were lazy, but obviously that wasn’t usually true, and those homeless people need direct fiscal help

price gouging is bad because it’s wrong to take advantage of people in emergencies

But I didn’t know anything about aggregate demand, or the costs/benefits of expansionary fiscal policy, or poverty traps, or prices-as-signals. I’d basically just absorbed sentiments from my political upbringing—I recently noticed that I disliked “supply-side economics” without even knowing what that is! These sentiments were sometimes mostly right, and sometimes incredibly wrong.

This book brought me two benefits. First, it introduces important frames for thinking. Second, it has lots of interesting facts and compelling philosophical arguments.

So let’s go.

The prisoners were dying of scurvy, typhoid fever, and smallpox, but nothing was killing them more than bad incentives. In 1787, the British government had hired sea captains to ship convicted felons to Australia. Conditions on board the ships were monstrous; some even said the conditions were worse than on slave ships. On one voyage, more than one-third of the men died and the rest arrived beaten, starved, and sick. A first mate remarked cruelly of the convicts, “Let them die and be damned, the owners have [already] been paid for their passage.”

The British public had no love for the convicts, but it wasn’t prepared to give them a death sentence either. Newspapers editorialized in favor of better conditions, clergy appealed to the captains’ sense of humanity, and legislators passed regulations requiring better food and water, light and air, and proper medical care. Yet the death rate remained shockingly high. Nothing appeared to be working until an economist suggested something new. Can you guess what the economist suggested?

Instead of paying the captains for each prisoner placed on board ship in Great Britain, the economist suggested paying for each prisoner that walked off the ship in Australia. In 1793 , the new system was implemented and immediately the survival rate shot up to 99%. One astute observer explained what had happened: “Economy beat sentiment and benevolence.”′

The story of the convict ships illustrates the first big lesson that runs throughout this book and throughout economics:

Incentives matter.

How do people decide what to buy and where to work, what opportunities to take and where to build? Microeconomics models decision-making by consumers and firms. Basic microeconomic models assume that people want to make money, and they’re good at it—they are rational. Unsurprisingly, this isn’t quite true, but the models let us easily think about what incentives people have in different situations.

(We can add corrections to the Econ 101 arguments later. I think this is better than throwing up your hands and saying “Econ doesn’t have all the answers, people are too complicated!”)

The most important microeconomic frame I deeply internalized was supply/demand curves.

Law of supply: Firms want to supply more pizza if you’ll pay them more; the supply curve is increasing.

Law of demand: Consumers want to buy less pizza if you charge them more; the demand curve is decreasing.

(Not all markets follow these “laws.”)

I significantly sharpened my understanding of incentives by internalizing how to shift supply/demand curves. So let’s reason through a contentious question with this frame:

I think price gouging should usually be legal (and most economists agree)

This section serves both as an epistemic spot check and an explanation I wish I’d read when I started learning econ. Skip if it’s old news to you.

Price gouging occurs when an emergency happens (e.g. a blizzard), people demand a lot of some good (e.g. snow shovels), and so stores jack up the prices (e.g. $4 → $30).

Consider a competitive snow shovel market, where firms can price shovels as they please (or, far more accurately: in response to economic conditions). When demand increases for snow shovels, that’s a positive demand shock because people want to buy more shovels. The demand curve moves out to the right, from D to D’:

Because people want more snow shovels, the price increases from to . (This is the “price gouging” part.) So here is the painful part of the picture. Now snow shovels are expensive, and some people can’t afford them, and also fuck you to the people taking advantage of a disaster just for a few bucks. Many people have this gut-level reaction.

But what comes next? Suppose the storm hits Wisconsin. Demand goes up, so prices go up. Since firms want to make money, suppliers in neighboring states (e.g. Iowa and Illinois) will start trucking in snow shovels and selling them at a high—but slightly lower—price. In fact, the hardest-hit areas with the highest prices will get prioritized for more supply, so that firms can make more money. As more firms enter the Wisconsin snow shovel market, they compete over price and eventually the price settles back to the original as demand subsides.

Prices are signals about which places want which goods, and free markets maximize social benefit when firms make money by responding to those price signals. The high price of snow shovels is like a huge neon sign which spells hey if you bring more snow shovels here you can make a lot of profit!

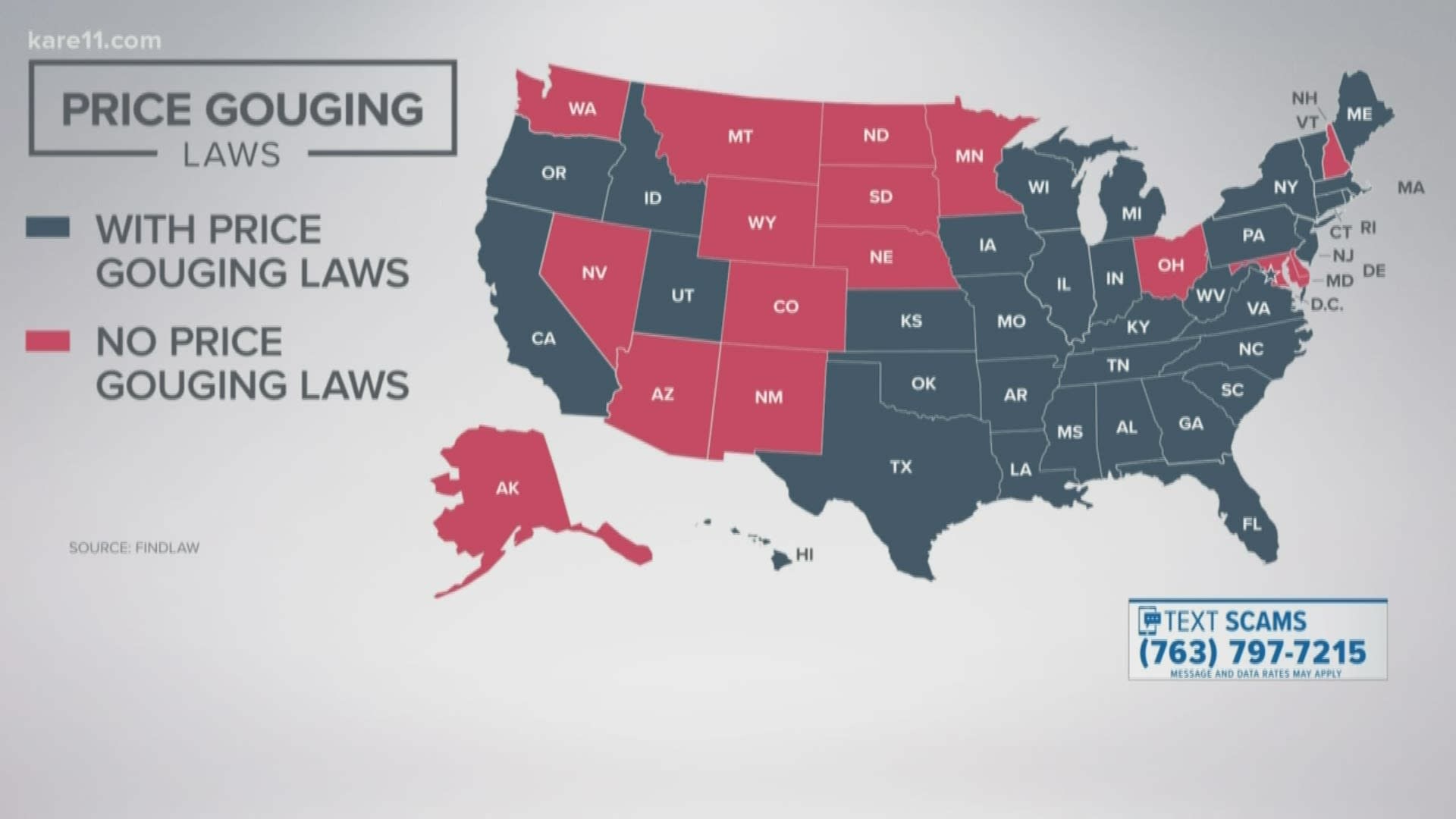

Some laws ban price gouging. In certain industries and during an emergency, firms basically can’t raise prices unless they can prove that their operating costs / input costs increased.

Suppose that the snowshovel price can barely increase from due to a so-called price ceiling.

Then there’s a shortage, because more people are willing to buy shovels at (what a deal, especially in an emergency!) than suppliers are willing to sell at . There’s no economic incentive for them to increase production, and incentives matter. But set aside profit-making for a moment.

The price signal—that big neon sign—is no longer present. Suppose you own a chain of shovel stores throughout the midwest USA, and all you care about is getting shovels to people who need them. Several cities all got hit by the winter storm. Which one needs the most shovels? How many?

Because there’s a price ceiling, you can’t tell. So you send more shovels to all the cities, but some get too many shovels and some get too few. The shortage remains, and people can’t get enough snow shovels, but at least they aren’t getting cheated, right?

In the price-gouging world, yes, some people pay more for shovels. A key issue seems to be inequality: Many poor people won’t be able to afford shovels. But price-gouging has several benefits:

Firms profit by supplying more shovels

Firms know which areas need shovels the most, because they’re the areas with highest prices

People with the highest willingness to pay will pay higher prices, ensuring that shovels don’t get misallocated to people using them for trivial reasons

In shortages, people don’t pay extra money, they pay extra time. They pay search costs as they drive around town and look online for places with shovels. In fact, the rational consumer pays up to (willingness to pay—artificially low sticker price) in search cost, erasing the supposed benefit to consumers.

At least a bribe has someone getting paid! Consumer time is wasted.

Who do you think has the ability to drop everything and run to the store to get a few shovels before they’re all gone? Are they probably poorer, or probably more wealthy?

So it’s not clear that anti-price-gouging laws even help poor people.

(Since people hate price gouging so much, large firms like Wal-Mart may decide not to raise prices and just sell out to preserve reputation, while smaller vendors gouge away. Thus you can get the “best of both worlds” without anti-price-gouging laws.)

I note that this picture assumes a competitive market; in particular, other firms can enter to sell shovels and compete to drive down prices. If that’s not true, then I think that the arguments for price gouging are much weaker.

The best argument I can think of against price gouging is that people are probably more irrational and manipulable during an emergency. I don’t think this overrides the other benefits of price gouging. I looked around for other counter-arguments and didn’t find any I thought were good.

So that’s the theory. How do things work back on planet Earth?

The empirical situation lines up with the theory.

These results support standard economic theory regarding price ceilings and counter political rhetoric in support of anti-price-gouging (APG) laws. When APG laws bind, counties may also experience shortages, increases in the total price paid for goods and services due to waiting time, and adjustments on non-price margins such as quality adjustments, the development of black markets, and rationing by violence.

— The Effects Of Anti-Price-Gouging Laws In The Wake Of A Hurricane

Remember the toilet paper hoarding of early 2020? APG laws are partially to thank.

The bottom line is: In an emergency, there won’t be enough shovels for everyone to get a shovel at standard price. If you want a long shortage, if you want to feel moral and avoid being blamed—outlaw price gouging in competitive markets.

I’m sure you’ll be absolutely shocked to learn that lots of states make price gouging a criminal offence.

How do demand shocks ripple?

By this point in the book, I’ve pinned down supply/demand curves. This was actually a bit tough, because I got caught up in the dynamics of how e.g. demand shocks in one industry would ripple through the economy. The answer was: Don’t worry about it. That’s much harder. Just focus on supply/demand curves, and everything will be OK for now.

Determining tax incidence

Another great mental motion is the “wedge” trick for tax incidence determination.

Think of the tax as the difference between what the consumer pays and the seller receives. Tax incidence answers: How much does the consumer pay, and how much does the seller receive?

The “wedge trick” is this. Consider a vertical line segment of length 6 in the above charts, and imagine it floating in from the left until it hits S1 and D with its endpoints. This determines tax incidence: The supply curve shifts up to S2. (This is actually the same as just shifting up S1 by $6, but I find it easier to visualize.)

If demand is more elastic than supply (aka the slope is less steep), then consumers bear more of the tax burden, and vice versa. The intuition is that it’s harder to tax people who are more ready to stop consuming/producing the product.

Surprisingly, statutory incidence—who writes the check to the IRS—doesn’t matter. The tax incidence is the same whether you charge consumers $6 more for buying cigarettes, or producers $6 more for selling cigarettes.

Other updates

Before I talk about the book holistically, here are more snippets:

The much-maligned capitalism is actually probably the greatest incentive alignment success in human history.

This is the whole point made by the “invisible hand” idea: Competitive markets “invisibly” have each firm produce until price equals marginal cost, and this minimizes total cost to society. While each firm pursues selfish interests, they advance societal goals by creating huge amounts of value in order to make money.

(Just think about how much you’d be willing to pay for glasses, and how much you actually have to pay! And that market isn’t even that competitive! Isn’t consumer surplus amazing?)

Rent controls are bad. Controls on competitive markets are generally bad.

I gained gears-level models for when government should or shouldn’t be involved in a market.

Sweatshops are bad but probably better for children than whatever else they would have been doing.

The Econ 101 argument goes: If the children had something better to do—like go to school or work at a safe, well-paying, age-appropriate job—they would do that instead of working at the sweatshop.

A firm perfectly price discriminates (PPD) if they charge each consumer their willingness to pay for a good. I really hope that firms don’t somehow achieve PPD via AI before the singularity. That would really suck. You’d basically be just on the edge of every single purchase you make—exhausting. And producers would gobble up surplus from consumers, which seems unfair.

Custodians in the US have higher real wages than custodians in India, even though they may be equally good at cleaning. This is because American custodians are more (economically) productive since they work for more productive firms.

The marginal product of labor (MPL) is the revenue from hiring an additional worker.

A custodian at Google is adding more value than an equally custodian at a small Indian firm.

Therefore, they have higher MPL, and are paid more.

Concretely: American custodians average $30,906/year. Adjusting for Indian purchasing power parity, that’s equivalent to rupees. The average Indian custodian only makes ₹120,726/year—less than a fifth the American wage.

Your wages aren’t just determined by your skills and your work ethic, but by the rest of the economy. It pays to work in a wealthy economy!

I had looked forward to learning about fractional reserve banking, ever since HJPEV reflected on the crudity of the Gringotts banking system. “What a sophisticated-sounding economic idea”, I thought. “I’ll need to study carefully to understand that one day”, I thought.

I thought wrong. Fractional reserve banking is stupidly simple. Banks keep a fraction of deposits on hand as “reserves”, in case customers want to make withdrawals. The rest of the deposits are loaned out. These loans put the money to work, growing the economy with people’s savings while also ensuring that people can withdraw their money.

This is why “just lock your gold underground” Gringotts is dumb: The wizarding economy could be growing using some of Lucius Malfoy’s money. Lucius, Gringotts, and the economy would benefit from this arrangement.

This is a general pattern: The key concepts in economics do not require nearly as much mental scaffolding as math concepts do. (Try explaining topological continuity in three sentences.)

Applying economic reasoning is still a delicate endeavor, though.

I now know what the Federal Reserve is and what they do.

And I now appreciate how hard central banking can be.

And I now appreciate how great it is that we let actual economists run this part of the government. Even if they sometimes mess up.

And I now appreciate this huge body of literature on interest rates and quantitative easing and M1 and market monetarism and agh! I’d always consigned the finance section of the paper to “inscrutable garbage that daytraders worry about”, but it’s so much more. I can’t wait to keep learning about macroeconomics.

The fact that wages are sticky-down is so annoying. I would be so mad if I were a central banker: dumb human bias ruining our ability to deflate! Dumb human bias making negative AD shocks horrible!

The dumb bias seems to be nominal wage confusion—responding to the dollar amount on your paycheck (the nominal wage), instead of to the goods you can buy with the money (the real wage).

In a negative aggregate demand shock, nominal GDP growth decreases. Normally firms could just lower wages for all their employees and real output would remain the same. But people hate hate hate seeing nominal wage cuts, and so it’s easier for firms to just fire people, or at least raise real wages far more slowly than inflation.

Which cuts actual growth in the short run.

What a mess.

Reflections

I’m very glad that I’ve used Anki. I probably made over 500 cards for this book, not only for the key vocab but also for charts, for brain-teasers, for cool pieces of reasoning the authors used. Cloze deletions are fast and convenient for all of these purposes.

This book is long. 800 pages long. It covers both micro- and macro-economics, and I was pleasantly surprised by the macro part. I’d heard macro is garbage, but I think it’s just less understood than micro.

investopedia and econlib are great resources for learning about economics.

It took a while for me to get comfortable with economics. At first, I felt uncomfortable and reluctant to read more, because everything seemed mildly confusing. Now I can read papers (with great effort) and have a good idea what they’re talking about. Learning more is now easy and fun; I’ve crossed the hump for economics in the same way I crossed the hump for mathematics.

I’m glad I read this book. It’s long, and maybe I could have skipped some of it. I didn’t get much out of the advanced indifference curve chapter; it wasn’t presented clearly. Most of the book was quite clear.

Conclusion

Economics is interesting, and powerful. Famine used to haunt most of the world, and now it doesn’t.

Famine seems to be the last, the most dreadful resource of nature. The power of population is so superior to the power of the earth to produce subsistence for man, that premature death must in some shape or other visit the human race. The vices of mankind are active and able ministers of depopulation. They are the precursors in the great army of destruction, and often finish the dreadful work themselves. But should they fail in this war of extermination, sickly seasons, epidemics, pestilence, and plague advance in terrific array, and sweep off their thousands and tens of thousands. Should success be still incomplete, gigantic inevitable famine stalks in the rear, and with one mighty blow levels the population with the food of the world.

— Thomas Malthus, 1798. An Essay on the Principle of Population.

Appendix: Open questions I have

I haven’t seriously looked into these questions yet.

What’s going on with market monetarism and quantitative easing?

In particular, I still find open market operations confusing for some reason.

Why isn’t the risk-free rate subtracted from capital returns?

I suspect this is just government being dumb.

Why aren’t all contracts indexed to official inflation estimates?

Wouldn’t this significantly cut down on arbitrary wealth transfers from inflation/deflation?

TIPS is indexed. What else?

This can’t be explained by dumb government; contracts are private.

Why do firms in a cartel have individual incentive to raise price above competitive?

IE: Why isn’t competitive pricing a Nash? If one firm unilaterally raised prices, wouldn’t the other firms just sell more in their wake?

What is the shadow banking system?

Study the impossible trinity of international economics.

How does free banking work?

FN: SRAS. Talk about some awful upwards-sticky prices; I wonder what the effect on SRAS is? I’d guess that ceilings probably aren’t binding for long enough to show up much macroeconomically.

Thanks to LessWrong for feedback on this post.

Sweatshops are nice, but not because poor workers prefer them to the alternative. After all, poor workers will also work in diamond mines or banana plantations, if the alternative is starving. But an economy based on diamond mines or banana plantations will always stay poor with bandits on top, while countries with sweatshops (trading their labor instead of extracting stuff from the land) get massive economic growth and “graduate” from sweatshops pretty fast.

About price gouging, I’m not sure this is even the right question. Disaster recovery is the perfect situation where planned economy beats market: there’s a known need, affecting a known set of people equally, and the government has tax money specifically for this need.

From what I remember form my history of Finland classes, the 19th/early 20th century state project to build a compulsory school system met some not insignificant opposition from parents. They liked having the kids working instead going to school, especially in agrarian households.

Now, I don’t want to get into debate whether schooling is useful or not (and for whom, and for what purpose, and if the usefulness has changed over time), but there is something illustrative in the opposition: children rarely are independent agents to the extent adults are. If the incentives are set in that way, the parents will prefer to make choices about their children labor that result in more resources for the household/family unit (charitable interpretation) or for themselves (not so charitable). Number of children in the family also affects the calculus. (One kid, it makes sense to invest in their career; ten kids, and the investment was in the number.)

Seconded. If a child going to school is better for the child but a child working in a sweatshop is better for the parents, some children are going to end up in sweatshops.

It’s not necessarily clear that disaster relief is better handled by the government. A few things to keep in mind:

It’s not a choice between markets or government. You can have both. (e.g: The army and rescue services organizing huge logistics efforts to resupply effected regions/clear roads. At the same time supermarkets are allowed to sell goods at inflated prices, incentivizing them to store a surplus in future cases where disasters may happen as they can make a profit large enough to offset the cost of keeping excess stock in inventory.)

The same incentive problems that apply to gov’s generally also apply here. A shop owner, assuming price gouging is allowed, is incentivized to keep a small surplus of disaster items in stock even though they won’t sell in normal times because of the small chance of an extraordinary profit if a disaster strikes. The government, even thought it should ideally keep track of and prepare for disasters, often won’t due to it being in no individual’s interests to do so. e.g: Lack of food stockpiling in New Orleans prior to Katrina.

It’s clear that something has lifted billions out of poverty, or at least from worse poverty into not-so-awful poverty. (At least, I think it is, but I’m not more than say 95% confident that graphs like the one here aren’t misleading because of e.g. imperfect inflation-adjustment of old and new income levels.) But how do we know that what did it is good economic policy?

(Some other possibilities: it could be the result of scientific and technological progress: Borlaug’s semidwarf wheat, or computers, or digital telecoms, or whatever. It could be the result of political changes: poorer countries gaining independence, or something to do with the rise and/or fall of communism, or the spread of democracy. It could be a sort of spillover from growth in the richest countries (which in turn could be good economic policy, or scientific/technological progress, or political change). It could be some sort of memetic-evolution thing: maybe there are certain ways of thinking that tend to result in economic growth, and they’ve been spreading; cf. the Flynn effect.)

I agree that there are other factors. As I wrote:

Some generators for my being bullish on economic policy:

Some economic historians point to capitalism as one of the key ingredients of the industrial revolution,

Also seems like the US was heavily influenced by Adam Smith and that that influence later proved quite fortunate, but I don’t know the exact part of the book which made me think that.

the fall of mercantalism roughly seeming to line up with industrial revolution,

the industrialization and opening-up of China tightly correlating with Chinese poverty dropping like a rock,

the fact that bad monetary policy stifles growth (see Japan until recently)—therefore, good monetary policy allows growth,

various comments I read in the book about the relationship between openness to trade and real GDP growth,

various comments I read in the book about the state of empirical economics.

I’m open to having overstated the case or missing considerations here or having been a bit sloppy in my reasoning. Those are just some considerations informing my current viewpoint.

I invite you to read my newish post on the Solow-Swan model of growth. After reading it, it will still be unclear how much economic policy has contributed to growth, but the ways that economic policy can help will likely become clearer.

Very broadly speaking, the main ways to grow an economy focus on technological development and capital accumulation. I still need to finish writing the post on endogenous growth theory, but the rough story there is that economic policy can help firms develop technological innovations.

As an interesting epistemic spot check, I’ll ask you a question: how much faster do you think the capitalist economy of the United States grew compared to the Marxist-Leninist Soviet Union?

The answer: GDP per capita grew at roughly equal rates until the 1980s, after which the Soviet Union entered a deep depression. Is that surprising? It might be if you think that growth is a direct function of how capitalist a nation is, or how much a nation listens to the advice Western economists. But that’s not the best model.

Growth depends on a variety of factors, in addition to economic policy: how far a nation is from the economic frontier, the presence of war and organized crime, and exogenous factors like climate and natural resources. There’s some really interesting stuff to learn about in growth economics.

I also like the Solow-Swan model. But if I’m evaluating “how can economic policy help growth?”, I can hardly do that from within an idealized economic model. The question is empirical, or at least empirical work must first support the predictive validity of the theoretical model. So I could have said “Solow-Swan makes intuitive sense, and makes decent predictions”, except I didn’t add it because I hadn’t heard that the latter was true. And I haven’t looked yet, either.

I guessed about 5x GDP/capita growth in US, both because post-war US was growing extremely quickly, and I hear that Soviet Union policy sucked (but I haven’t looked closely). So I was surprised, but my (implicit) model wasn’t “capitalist->more growth”, it included considerations like “weaker property rights decreases individual incentive to invest, decreasing the Solow steady-state equilibrium output” or “centralized planning leads to huge deadweight loss, misallocated production, and underspecialization.” So I still am surprised and confused.

I disagree. Idealized models can help by answering what happens when we intervene on one of the variables. For example, there are policies that can increase the national savings rate, and thus increasing capital accumulation and per capita output (like the 401k). The Solow-Swan model doesn’t directly state how to do this, but you can endogenize the savings rate; the most famous attempt is the Ramsey–Cass–Koopmans model, which shows how households make tradeoffs between savings and consumption, and helps us see we might intervene to affect the savings rate.

FWIW, I think “strong property rights” is the defining feature of what most people consider “capitalism” so I don’t see these as separate models.

I think there was an opportunity for the USSR to grow faster, on par with other countries that leapfrogged it since the 60s. Maybe it’s not about capitalism vs socialism, but still has to do with economic issues, like the oil curse.

The picture looks like evidence there is something very weird going on that is not reflected in the numbers or arguments provided. There are homeless encampments in many countries around the world, but very rarely 20 min walk from anyone’s office.

Yeah, I liked the post overall, but the rest of it seemed entirely unrelated to the picture and the claim that this is a success story for economics. I was expecting it to come back and explain the connection, but it seemed to never do.

The intended takeaway was “availability heuristic can deceive you; growth is real and important; if you just look out the window you might miss it.” There are some polls (which I can’t find after a minute of searching, unfortunately) showing how most Britons perceive extreme poverty to be increasing, which is just wrong. (At least, definitely wrong before COVID, maybe COVID was a shock for this metric)

Okay. As someone living in a major city where street homelessness has mostly been solved, it doesn’t manage to convey that message to me. Even if there’s been more growth than the sight of those people might suggest, the growth clearly hasn’t benefited them as much as it has benefited homeless people in places that seem to have better policy.

Thanks. I added a bit to the transition between the encampment photo and the charts. Hopefully the intended message is clearer now.

Cool, it is! :)

My cached answer is “Bay area zoning”, but I honestly haven’t looked into it in great depth. There’s a 3-tent encampment literally 20 seconds from the office where I’m at right now in downtown Berkeley.

I think overregulation of land is indeed responsible for high rents and many other problems, but it’s not the main factor in homelessness. Many Western cities with high rents still have much fewer homeless than the Bay Area. There are counterexamples in the other direction too: Moscow in the 90s had a lot of questionably legal construction and a lot of homeless.

Maybe the Bay Area homelessness situation is caused by US society being unwilling to house and feed the homeless in cheaper areas? That might be a simpler explanation, but I don’t know enough.

Better-for-them or better paid? Going to school can easily increase your lifetimes earnings, but had upfront costs. That’s a 101 claim that’s particularly in need of enhancement.

I agree that the distinction is important. The argument is that if there were a way to have the child do something nice, the sweatshop wouldn’t have to close down for that to happen. If I had to guess, extremely poor families do not have the slack to increase lifetime earnings by delaying immediate income from their children working. The book noted that subsidizing families who send kids to school does decrease child labor, while embargoes on sweatshops does not (IIRC).

If that’s the case, I believe it illustrates a failing of economics. If there are enough resources available in the country for every child to go to school and their families to still eat, but only the top (say) 20% of children can go to school, and the bottom 80% must work in order to economically justify their families receiving food, then everyone loses in the long run. Yet, the people who make the food have no individual incentive to give it to the families of the children, unless they work...

To clarify: when you say “a failing of economics”, do you mean something like “there must be bad economic policy going on here”, or something more like “the field of economics is failing to make correct predictions”?

I recently finished reading the book with a small group of friends. One thing we all thought was that the micro half of the book was far better written then the macro half. We all came away from the micro half with a clear, intuitive understanding of most of most of the concepts explained. On the other hand the macro explanations seemed to be both more complex and also less persuasive. There were a number of times we thought up obvious objections to a macro explanation, expected the book to cover it only to find that it moved on.

one argument against price gouging that I don’t see bringing up is the 2nd order effect.

I acknowledge that price gouging can have multiples benefits and act as signal and preventing price gouging would inhibit market’s direct action.

However, forbiding price gouging also disincentivise agents from creating conditions that they can gouge others.

one extreme example: if I can price gouge water, I will be incentivised to go around poisoning all other water source to sell my water at a premium.

since I can not sell my water at a higher price, I am not incentivised to destroy water resource.

This also applies to the sweatshop example. If everything else is fixed, then yeah, probably those poor families are better off being allowed to work in awful conditions for low wages. But everything else isn’t fixed.

When a bunch of relatively wealthy and powerful people are benefiting financially from the existence of an extremely poor underclass (who, due to their poverty, are willing to do hard unpleasant work for little money), this creates resistance to reforms that would improve the situation of the poor and thereby give them greater bargaining power.

And, slightly more optimistically, the alternative to sweatshop employment might not be as dire as it seems. When people are literally at risk of starving for lack of work, there tends to be greater political and charitable will to help them, compared to when they’re out-of-sight out-of-mind doing something unpleasant but useful.

The wealthy may benefit from the existence of low-skilled labour, but compared to what? Do they benefit more than they would from the existence of high-skilled labour?

Yes, they benefit from low skilled labour as compared to no labour at all, but high skilled labour, being more productive, is an even greater benefit. If it weren’t, it couldn’t demand a higher wage.

Even without sweatshops that produce products for Western audiences, the wealthy in a given third-world country still profit from cheap labor.

Most communities that have sweatshops also have people who are at risk of starving. It would be surprising to me if there are those dynamics that a closed sweatshop leads to significantly more political and charitable help in the region. Do you know of any case studies where a sweatshop closed and that resulted in increased political and charitable help?

You can sell more water at the same price. So the incentive is less, but not zero.

good point, I would amend that to reducing the marginal incentive to go around poisoning water source then

This is worth considering, but I basically expect the rest of the legal system to disincentivize this hard enough, and it doesn’t seem obvious that firms can tacitly create these conditions in order to create plausible deniability (as they can with eg tacit collusion).

I am not sure how true is this, but my friend in comsumer protection agency told me that after a particular severe weather event there were a conspiracy to raise roof repair price between most trade workers in the area by not competing on price before the agency crack down on it.

Not even sure if the crack down had any effect to be honest.

I can see the argument that this is natural price raise due to increase demand, but look at it another way it could be seen as artificial reducing supply to increase price.

Referring to the “criticism of these numbers” arguments: the only one that stands out to me as very serious is 5. From my reading history and historiography, the problem of quantifying changes among groups of people who mostly practice subsistence farming and do not have any records of birth, health, death, or productivity is notorious. It looks to me like it would be down to archaeological and anthropological data to determine what their lives were like, and then the comparison with the lives of people on $X/day could begin.

I wouldn’t go as far as calling the numbers bullshit, but wew lad do I expect the error bars to be huge on the early end of that chart. Time to go digging through those links to find out what they actually did!

Edit: yep, that’s the case. They took the extant work from historians using the archaeology/remains methods and combined them as well as they were able. I was interested to see that the highest-uncertainty parts aren’t so much the earlier periods as the periods where completely new products or radical product quality changes were introduced. So if we were to see the uncertainty, I expect it would start wider at the beginning and narrow as time went on, with spikes during stuff like the introduction of vaccines or factories.

presumably perfect competition defects from perfect price discrimination

I agree with most of this. But it also needs to be said that a problem with free market is externalities; the legibility and accountability of side effects of the market transactions.

Factories generate pollution. The official part of the transaction is that the customers can buy widgets that improve their lives, and the factory owner gets rich. The side effect is that people living near the factory get cancer. The only thing needed to make this transaction happen is that the benefits of the customers exceed the costs of the producer; the costs of the cancer victims are not included in the equation.

That reminds me of another thing that is super unproductive by the same logic: providing services for poor people. An effective altruist might tell you that money used to cure one rich person could instead be used to cure hundred poor people; but an economist might respond that there is actually a good reason why we are already not doing that.

Interesting things happen when free market interacts with things that do not follow the rules of the free market. For example, if some products are produced using slavery, they can be further distributed on the free market, making all market participants more rich… which is an incentive for some of them to capture more slaves.

Externalities are indeed important and well-covered by the book. My review is not comprehensive.

True, but also the economist may or may not mean “good” in a different sense than goodaltruism.

I am forced to wonder why no generous individual has thought to go down to the hardware store, buy maybe $200 worth of materials, and build those guys a better bigger (crude) shelter and some crude furniture. I suppose the police would come along and knock it all down and arrest the person who did so.

Yeah, I am remembering a YouTube video, or maybe a documentary about this. It was exactly as you describe. Some generous individual had invented a type of pop-up home, something in between a tent and a super small home. They would go around building/giving them to homeless people, and the police would indeed knock it down. I don’t recall the police ever trying to arrest anyone though.

That’s the reason central allow cation fails in theory? Des it fail in practice? If you’re a government or an NGO you have statistics available about how many people live in an area and are affected by what.

And what’s the worst case of misdistributing supplies? The worst case is that some people die. What’s the worst case of price gouging ? The same .

It’s not just inequality, it’s potentially fatal inequality.

You say “manipulative” like it’s a bad thing. During emergencies, people manipulate each other into being more altruistic, and altruism aids group survival.

Agreed. And yet—what shall we do about the people who can’t buy shovels at all because there’s a shortage? Price gouging is blame-able (you can actually see someone having to pay a lot for a shovel), but people don’t see the counterfactual shovels that are not there due to bad policies.

It’s not like no ever thought about this. Governments and NGOs can buy things and stockpile things and distribute things.

When there is a shortage of shovels, we should employ rationing, which is a valid alternative to price gouging that many people seem to forget about. Yes, maybe one family would like to buy 20 shovels if they are $10 each. Tough. They get one, just like every other family. This especially applies if it is a short-term shortage which the market wouldn’t be able to re-equilibrate before the shortage was solved another way (by the storm going away and the roads getting fixed).

Unless absolutely ludicrous prices are charged for the shovels, the utility for each family having one snow shovel is much greater than the utility for half the families having no shovels and the other half having two.

The major shortage we have in many cities today is housing. Some cities pass laws saying nobody may charge more than $XXX/month in rent, and that doesn’t work. But smarter cities pass laws saying nobody may raise rent more than $XX/month/year, nobody may evict a tenant just to get higher rent, and for new buildings people can charge as much rent as they like. Then there is no supply disincentive!

Also on price gouging:

Sure there is, so long as the price ceiling allows some level of profit per item.

If obtaining more of the good at its normal cost could fix the shortage, it wasn’t a very severe shortage. The serious ones do require obtaining more units of the good at higher cost per unit, one way or the other. Imagine a drought that makes bread production more expensive, or a snowstorm that increases transport costs for bringing snow shovels from the next town over.

As I said in the other comment, if society feels that some good should be offered for cheap to people in need, then it should actually offer that good for cheap, funded by taxes. Banning private actors from offering that good at higher price is just an empty way to pretend you’re helping.

So what’s stopping you obtaining more of the good at the normal cost? The fact that it is not profitable to make more of the good was offered as a reason, but it’s not actually true in general.

Edit:

You can’t take the fact that price rises happened to mean that they were necessary.

That’s how you end up with the US medical system: everyone has to pay a lot, including the taxpayer,who has to fund other people’s expensive healthcare.

If the taxpayer is forced to buy something, they can reasonably hope that it is being obtained cheaply.

Looking at the graph immediately following seem to over state the shortage or require the assumption that the set price ceiling in fact ignored the clearly demonstrated (S curve) increase in costs. If we move to the view that the administrative price is well informed then you just get market clearing. The argument there should be no gouging is occurring—that would just be the uninformed rhetoric.

I suspect the real problem with attempts at price gouging all relate to attempts to restrict supply (at least in some local, short term aspect). Early in the pandemic days when all the store shelves were empty of some items there was a story about some guy that had a garage full of some item (forget if it was disinfectant wipes, toilet papers or what—one of the high demand items). He had bought out the supplies early with the intent on selling at a high profit when supplies were even tighter. So the dynamics of price gouging and the profit motive can lead to some perverse outcomes that are not consistent with what you could call efficient or welfare positive market outcomes. Of course this is not some new behavior—used to be called front-running and was consider a violation of the terms of many of the old Merchant Guilds in European history.

Side note on prices as signals. While I’m generally very sympathetic with the prices are signals view, it’s not always obvious to infer just what is being signaled. Generally the claim is increasing prices should signal need for more supply while falling prices signal a need for less supply. However reality seems to allow for the reverse to be the case. Declining industries with fixed costs in production will likely see increasing prices as demand falls and suppliers exit—strange case of being on a negatively sloped portion of the supply curve. Similarly, increasing demand with fixed costs also allows for prices to fall as the increased output takes advantage of the economies of scale from fixed costs in production. Not looking into the details and taking the signal at “face value” would lead to a really bad investment in the first case. In the later case it might lead to missing a great investment.

If he bought the supplies earlier, then he creates a signal to the producers of those suppliers at the time of his purchase that they have to produce more. That’s good.

There’s also a good chance that the toilet paper he sold was on average more valuable to the buyers then the toilet paper was to those buyers when he brought his supplies.

I think stories like those during the Texan blackout (https://www.cbsnews.com/news/texas-power-outage-griddy-lawsuit-electricity-bills-2021-03-26/) are a better example for problems that might be prevented by some price regulation.

The market can remain irrational longer than your bum can stay free of shit.

I will just note that you are making a quantity argument here, not a price argument.

It was two guys and hand sanitizer.

https://www.today.com/news/brothers-who-hoarded-17-700-bottles-hand-sanitizer-forced-donate-t176028

I remember it being discussed on /r/themotte. The 101ists were staunchly defending it , but the professional economists in the discussion were much less impressed.

On sticky nominal wages: any attempt to overcome this bias has to deal with the entire mess of existing financial obligations that people take on which are denominated in fixed nominal dollars. My mortgage payment is fixed for the next thirty years in nominal dollars, an arrangement predicated on longstanding assumptions about average future price changes. My car payment, similarly fixed for five years. If prices of everything go down by some percentage, my single largest expenses don’t change, and so a comparable change in my nominal wage could easily be devastating. And if the prices of houses go down, I can’t even sell my house and buy a different one b/c I might not make enough on the sale to do so after paying back the existing mortgage. What proposals have been put forward that might overcome this?

But when the Titanic was sinking, the insufficient lifeboat spaces were allocated to women and children. Would it have been better to offer them to the highest bidder?

That wouldn’t have led to more lifeboat spaces being produced. (Whereas one of the key arguments against price ceilings and the like is that allowing prices to rise does lead to more of whatever-it-is being produced.)

It wouldn’t have led to more lifeboat spaces being transferred from other ships. (Whereas one of the key arguments against price ceilings and the like is that allowing prices to rise does lead to more of whatever-it-is being transferred from elsewhere where the need is less and therefore the price is lower.)

So the case of the Titanic’s lifeboat spaces is quite unlike (say) the case of surgical masks at the start of a pandemic, or the case of Uber taxi rides when there’s an event on.

(There are other cases that are more Titanic-like. For instance, government-imposed limitations on increasing rent; building new housing and repurposing buildings are relatively difficult, expensive, and slow.)

Except that its not the only way of incentivizing production. Ie, forbidding price rises doesn’t disincentivise production. Most businesses would be happy to sell more products at the same price.

I don’t think anyone was ever arguing that it’s the only way of incentivizing production. (There are others besides “you get to sell more at the same price”, too. A government could offer grants to businesses making whatever it is, or threaten penalties for businesses that could make them but don’t.)

Any given combination of potentially-incentivizing mechanisms will produce some level of increased production. So the question is: how much production do you get, and therefore how much of the relevant thing do you get to the people who need it, with different combinations of mechanisms, and how does that trade off against the downsides of those mechanisms (free-market prices mean that poorer people have more trouble getting the thing; government grants mean that the government needs more money from somewhere, probably taxation; any government intervention risks getting the required quantities wrong; etc.).

Exactly how all this works out seems like a complicated question, but here are two key things from the OP: “most economists agree”, and “the empirical situation lines up with the theory”. Of course the first might just indicate prejudice on the part of economists or something, and the latter might be based on cherry-picked empirical evidence; if you have reason to think that either or both is so, I’m all ears. But the way it looks to me right now is: there’s a simple argument suggesting X should happen; fancier analysis (visible via opinions of “most economists”) and actual empirical evidence both suggest X does in fact happen; most likely the simple argument is basically right, and the various ways in which it’s too simple don’t end up invalidating it.

It’s the only one I can see mentioned in the OP.

You could argue that when someone says “X is good” they really mean “X, Y, or Z is good”...but I don’t have to believe you.

Does it? There’s plenty of evidence that heavy handed state intervention, like rationing and price controls work in emergencies.

I wasn’t arguing that when someone says “X is good” they mean “X, Y, or Z is good”; I was arguing that when someone says “X is good” they mean “X is good” rather than “X is good and Y and Z aren’t”. But, in fact, I see that TurnTrout did actually write “There’s no economic incentive for them to increase production” (in a situation where prices can’t increase), which I agree is wrong outside Econ101-land (because supply is a function of expected demand as well as price, so in situations of increased demand there’s an incentive to produce more even if prices can’t increase). I suspect that TurnTrout was being sloppy rather than outright wrong and didn’t really mean to claim quite what he did, but you’d have to ask him to find out whether my guess is right or not.

The first of the two specific bits of research TurnTrout quoted in support of the claim that “the empirical situation lines up with the theory” was specifically about emergencies, and it purports to find that heavy-handed state intervention is harmful in the emergencies it looks at.

(The second is about shortages of goods like toilet paper and hand sanitizer near the start of the COVID-19 pandemic, which is less emergency-like.)

But if you have particular research in mind that finds that anti-price-gouging laws are beneficial on net in emergency situations, I’d be very interested to know what it is.

If you end up being right about this consideration, it’s fairer to say that I was wrong, because I hadn’t thought of it.

But I don’t yet clearly see the argument. Competitive firms produce until P=MR=MC. If (expected) demand increases and there’s a binding price ceiling at P, the firm still has P=MR=MC and so extracts no economic profit from producing a greater quantity.

If MC is locally constant, then I suppose they could increase production without economic loss. But that seems bad because once the demand shock subsides, they’ll be stuck with too much production capacity and no one to sell it to, right?

EDIT: Another way I could be wrong is if short run supply were responsive enough to adjust on non-price dimensions, like lower quality same price, to drive up profit and produce more overall.

If you weren’t sure, you could just ask which I meant. gjm is right: I wasn’t claiming that gouging is the only way to incentivize production.

What about Cowan?

Maybe it would.

As far as I know, some lifeboats on Titanic were left half-empty. (Sailors insisting that women and children get the places first, women refusing to abandon their husbands, everyone wasting time, then the ship sank before all places were occupied.) Perhaps auctioning the places would lead to less chaos, and greater total number of people saved.

Supposedly they were (mistakenly) afraid of putting too much weight in the lifeboats?

Most of them wealthy men. The point of women and children first is about rebuilding a society.

The society outside of Titanic wasn’t in a dire need to be repopulated by the survivors from the ship.

And if they had the luxury of time, they might have been able to realise that. But they didnt have the luxury of time, and they didn’t have enough time to organise an orderly auction either.

Its all about what the default is. In an emergency, you cant hand craft a perfect solution. We are the descendants of people who have survived a lot of emergencies, so we default to things like “promote the group over yourself”, ie.”don’t guage” and “fertility counts more than accumulated wealth”, ie. “women and children first”.

Because, in general, they work.