AI looks likely to cause major changes to society over the next decade.

Financial markets have mostly not reacted to this forecast yet. I expect it will be at least a few months, maybe even years, before markets have a large reaction to AI. I’d much rather buy too early than too late, so I’m trying to reposition my investments this winter to prepare for AI.

This post will focus on scenarios where AI reaches roughly human levels sometime around 2030 to 2035, and has effects that are at most 10 times as dramatic as the industrial revolution. I’m not confident that such scenarios are realistic. I’m only saying that they’re plausible enough to affect my investment strategies.

Companies working on AI

Google’s DeepMind seems a bit more likely than any other company to produce valuable AI. That’s a good enough reason to hold a modest position in Google. TPU and Waymo are additional AI-related reasons for holding Google stock.

OpenAI is a serious contender. Microsoft has a $1 billion stake in OpenAI. But profits from that seem to be capped at 100x, so the best case scenario seems to be that Microsoft shareholders get $13.40 per share from that stake. Maybe Microsoft will invest more in OpenAI. I only see Microsoft getting a modest boost from AI.

Conjecture sounds quite promising. I offered to invest $100k in them this summer. They don’t seem interested in investments that small.

There are other new private companies that I haven’t been able to evaluate. Here are some that seem worth paying some attention to:

That’s a dramatic pace of new startups being founded that look potentially important. VC’s seem to have been throwing enough money at them in mid-2022 that they likely had little reason to talk to more ordinary investors such as myself. Investment in such startups has maybe cooled slightly now that FTX has stopped throwing money at them, but I’m guessing it hasn’t cooled much.

I see a 50% chance that one or more of these new startups will make DeepMind and OpenAI irrelevant. I have little hope of being able to buy a diversified portfolio of such startups, so I don’t expect to profit from direct investments in companies working on AI.

Computing Hardware Companies

The most promising investments involve the hardware needed to power AI. That mostly means semiconductors.

Semiconductor capital equipment companies seem more promising than companies that are more directly involved in making chips, as capital equipment is more cyclical, and less dependent on specific uses.

My current semiconductor-related investments are (in alphabetic order): AMKR, AOSL, ASML, ASYS, KLAC, MTRN, LSE:SMSN, TRT.

I’m likely to buy more sometime in 2023, but I’m being patient because we’re likely at a poor part of an industry cycle.

Others that I’m considering buying: ACLS, AMAT, INTC, LRCX, MU, and PLAB.

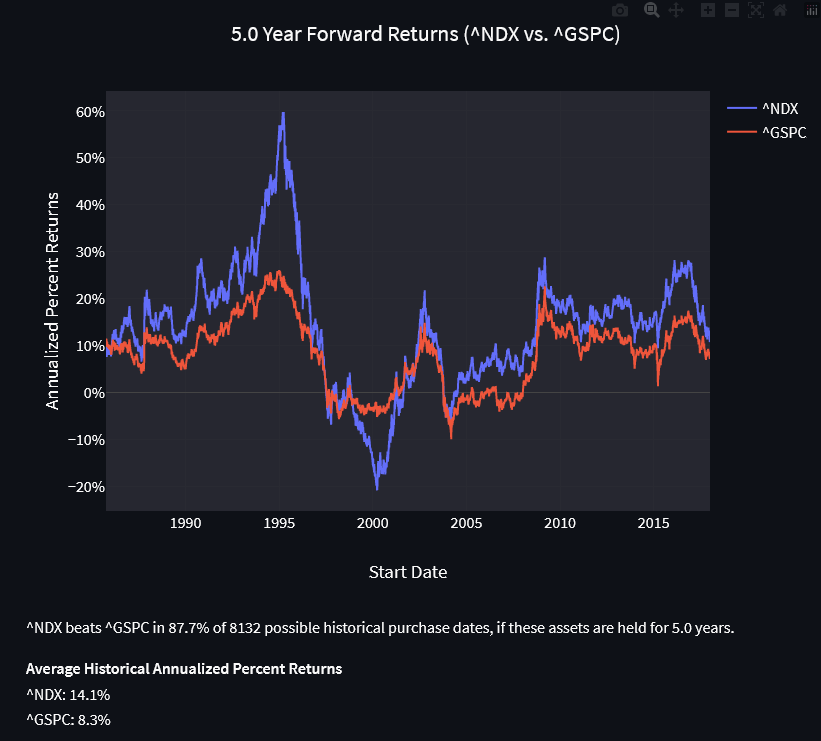

Some of you will be surprised that I didn’t suggest NVDA. Its PE and price/sales ratio are high compared to my other semiconductor investments. I can imagine buying it if its stock price drops relative to other semiconductor stocks. But I suspect its fans underestimate the risk of competition from hardware that is optimized more specifically for deep learning.

I’ve invested in privately held Fathom Radiant, which seems to have a shot at NVIDIA-like success in AI-related hardware. I’m unsure whether they’ll want any more investment in 2023.

I’ve seen some noise about neuromorphic computing. I suspect that such research is far enough from commercialization that it’s hard to figure out how to invest in it. (Also, I’m nervous about helping to speed up AI, as it’s already coming fast enough to worry me.)

I have a tiny position in Everspin Technologies (MRAM), mainly because of vague suggestions that their technology will support neuromorphic computing. I haven’t found much substance to that speculation, so I think of it as a real long-shot. Maybe a 2% chance of a 500x return this decade, without a high risk of the stock becoming worthless?

INTC also does some neuromorphic work, and seems to be a relatively safe investment even if it lags behind the cutting edge.

Datacenters

Datacenters seem likely to become a major industry, but I don’t see great investments here.

AMZN, MSFT, and GOOGL are likely to get some benefit from datacenter growth. I guess I’ll expand my GOOGL holdings and buy small positions in AMZN and MSFT sometime in 2023, when I see signs that their stock’s downward momentum has dissipated.

EQIX is an example of a company whose revenue growth seems likely to accelerate. But that will be capital-intensive, causing the company to sell enough shares that revenue per share growth doesn’t look very impressive. Also, its PE is high.

AAOI is a floundering company that gets over 30% of its revenues from selling products to datacenters. It might recover and profit from datacenter growth, but I’ll wait for its losses to shrink before buying.

Semiconductor stocks seem to be strictly better ways of benefiting from datacenter growth than datacenter-specific stocks.

Robotics

AI seems to be on the verge of turning robotics into a major industry. But it’s still hard to see when and where the key advances will happen. I suspect the main winners will be companies that aren’t yet public, as I’m not too impressed by the opportunities I see so far. I’m playing this mainly via tiny positions in LIDAR companies (INVZ, OUST, LAZR) and SYM.

I have a moderately large position in OSS, whose ruggedized computing products have some robotruck applications. I should look more carefully for other companies that make robotics-related hardware.

Energy

Electricity use is likely to become a larger fraction of the economy as AI takes off. AI is energy-intensive, and will catalyze much more digital activity.

Utility-scale solar seems likely to supply an important fraction of that additional electricity.

My two biggest solar bets are CSIQ, and SCIA. I have smaller positions in JKS, DQ, SEHK:1799.

For power grid infrastructure and solar farm construction, I have positions in MTZ, MYRG, PLPC, and PRIM.

I consider it somewhat likely that nuclear energy will somehow grow more important as a result of AI, but I’m pretty fuzzy on the details. Fusion is likely to be feasible in the 2030s, but I have little idea as to whether it will be competitive.

For fission, there’s SMR, uranium mining companies, and uranium futures. I haven’t invested in these, and I’m not in any hurry to decide which of these to buy.

Others

Here are some weak guesses about how AI will affect existing companies that make up significant parts of current portfolios, by industry:

banks: slightly negative—customers will shop around more for better terms, but the basic business looks relatively stable

investment banks, brokers, etc.: slightly positive—profit per transaction will decline as markets become more efficient; the total number of transactions will increase, possibly by a lot

homebuilders, real estate (REITs): neutral? I see relatively few effects here

casualty insurance: slightly positive—better risk analysis and understanding of contracts will cause more risks to be insured

life/annuity insurance: neutral?

pharma/biotech/hospitals/health insurance: negative? increased innovation may render existing companies obsolete?

chemicals: mildly positive, due to increased demand

mining: positive—possibly large increases in demand, which will be hard to offset by more efficient production

oil and gas: mildly positive, due to increased energy use; but oil stocks will be riskier, as AI will slightly speed up innovation in competing energy sources

aerospace and defense: I don’t know

autos: weakly positive? robocars will increase miles driven; profit margins likely decrease as cars increasingly bought by experienced price-sensitive buyers (Uber, Lyft)

trucking: positive—robotrucks will make it more flexible / convenient

shipping: mildly positive for oil tankers and dry bulk ships, mildly negative for container ships (robotic factories mean less reward for trade between high wage and low wage countries)

restaurants: neutral, but with increased risk? likely increased concentration into a few chains that handle robotics well (i.e. publicly traded chains prosper at the expense of smaller restaurants); increased competition from companies specializing in delivering meals to homes or preparing meals at home

fashion/clothing: negative—less IRL signaling, replaced by VR equivalents

electric utilities: negative? increased demand, but regulations ensure that shareholder returns are mostly unrelated to demand

We should also think about the effects of an AI-induced general increase in economic growth. Some of the biggest winners in that scenario will be commodified industries where capacity is slowest to change: oil and gas, mining, and shipping.

Other scattered thoughts

I see many changes coming that are hard for investors to exploit.

For example, many forms of therapy seem ripe for being replaced by AI. Most patients can’t find top-notch therapists. Therapists have little ability to document their successes. Even when they are able to get a reputation as a great therapist, they can’t scale up to serve more than a tiny fraction of the clients that need them.

AI can eliminate the latter problem. The reputation problem is much harder. If one out of every 10,000 patients publishes informative reviews of the AI, that will generate reputations that are much more informative than those of current therapists (assuming that fewer reviewers are actively creating noise).

If the system gets good enough feedback about the results of its advice, it will only take a few years to accumulate better knowledge than the top 1% of therapists. I imagine an AI therapist who has treated a few million patients will be able to usefully sort patients into thousands of categories, and, for the average category, the AI will have tried a dozen different approaches, and will remember which ones worked best. The AI doesn’t need an IQ of 100 to translate that specialized knowledge into a large advantage.

Some countries will adopt enough regulations that prevent AI therapy. Will they be able to prevent patients from learning about and finding ways to use AI therapists that are launched in other countries? I’m mildly optimistic, but not willing to bet much.

That might cause an important decrease in prescription drugs for mental health. It seems premature to short the relevant stocks, but I’m going to start paying attention to that area (see the new etf SANE).

I expect that in something like 5 years, several AIs will be created that are able, given enough capital, to make stock markets too efficient for me to be able to measurably outperform the market. Should I prepare to retire from this career? The “given enough capital” part won’t happen instantly. There’s lots of investment funds that will be slow to adopt AIs, and there are a moderate number of market inefficiencies that will remain until a lot of capital is mobilized to eliminate them. So I’m unlikely to retire as a stock market speculator before 2030.

Can I be one of the leaders in applying AI to the stock market? I plan to think more about this, but my current guess is that the superior access to large datasets of big institutions gives them too much of an advantage for me to compete with, and I’m not comfortable with joining one.

{kind=link}

I plugged the stocks mentioned in here into Double’s backtesting tool. I couldn’t get 6 of the stocks (Samsung, one of the solar ones, 4 other random ones). At least in 2024 the companies listed weighted by market cap produced a return of about 36%, being roughly on par with the S&P 500 (which clearly had an amazing year):

And he didn’t include NVDA, which went crazy. Bad choice: NVDA was the clear winner.

For reference, NVDA was hovering around $14.61 per share at the time this post was made.

It peaked at November 8th of this year at $147.63 per share, just slightly over a 10x increase.