How I Learned To Stop Trusting Prediction Markets and Love the Arbitrage

This is a story about a flawed Manifold market, about how easy it is to buy significant objective-sounding publicity for your preferred politics, and about why I’ve downgraded my respect for all but the largest prediction markets.

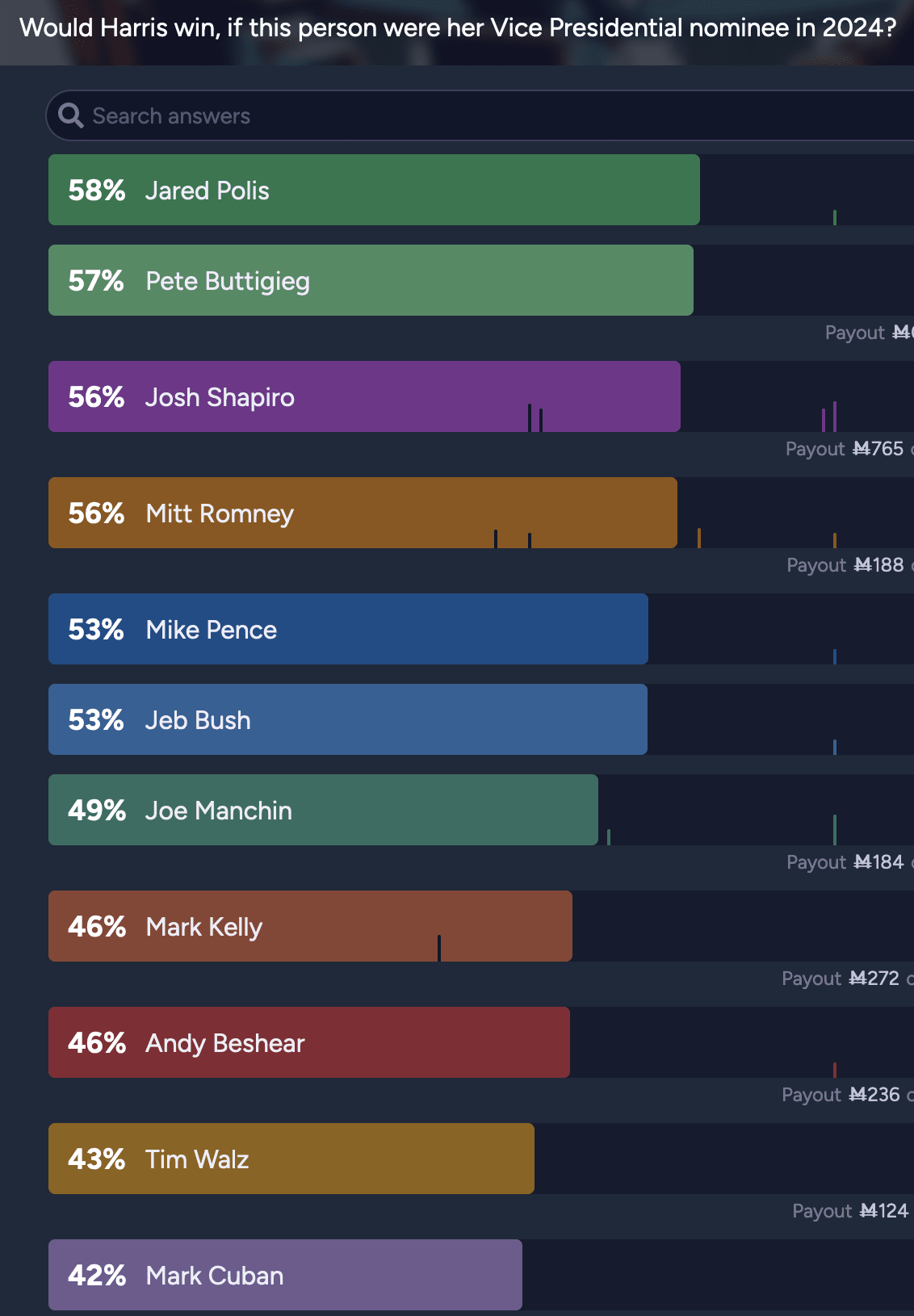

I’ve had a Manifold account for a while, but I didn’t use it much until I saw and became irked by the popularity of this market on the conditional probabilities of a Harris victory, split by VP pick.

The market quickly got cited by prominent rat-adjacent folks on Twitter like Matt Yglesias (who used it to argue that Harris should spend more time courting Never Trumpers), because the question it purports to answer is enormously important.

But as you can infer from the above, it has a major issue that makes it nigh-useless: for a candidate whom you know won’t be chosen, there is literally no way to come out ahead on mana (Manifold keeps its share of the fees when a market resolves N/A), so all but a very few markets are pure popularity contests, dominated by those who don’t mind locking up their mana for a month for a guaranteed 1% loss.

Even for the candidates with a shot of being chosen, the incentives in a conditional market are weaker than those in a non-conditional market because the fees are lost when the market resolves N/A. (Nate Silver wrote a good analysis of why it would be implausible for e.g. Shapiro vs Walz to affect Harris’ odds by 13 percentage points.) So the sharps would have no reason to get involved if even one of the contenders has numbers that are off by a couple points from a sane prior.

You’ll notice that I bet in this market. Out of epistemic cooperativeness as well as annoyance, I spent small amounts of mana on the markets where it was cheap to reset implausible odds closer to Harris’ overall odds of victory. (After larger amounts were poured into some of those markets, I let them ride because taking them out would double the fees I have to pay vs waiting for the N/A.)

A while ago, someone had dumped Gretchen Whitmer down to 38%, but nobody had put much mana into that market, so I spent 140 mana (which can be bought for 14-20 cents if you want to pay for extra play money) to reset her to Harris’ overall odds (44%). When the market resolves N/A, I’ll get all but around 3 mana (less than half a penny) back.

And that half-penny bought Whitmer four paragraphs in the Manifold Politics Substack, citing the market as evidence that she should be considered a viable candidate.

What About Whitmer?

There’s one name in that chart I haven’t mentioned at all: Gretchen Whitmer. The popular governor of Michigan, Whitmer was widely floated as an alternative to Biden and Harris. She said she didn’t want the job, but my read is that’s just something politicians say when they don’t think they’ll get it. So why isn’t she under consideration?

Well, it’s pretty obvious when you look at the other options, isn’t it? Since Harris is a woman of color, the conventional wisdom is that in order to win white swing voters in the Midwest, it’s imperative that she restore “normalcy” to the ticket by picking a white man — or, at the very least, it would confer some advantage. So far, by publicly considering only white men, she hasn’t shown any signs that she disagrees with this philosophy.

Matty Yglesias and Nate Silver do, though (among others). In Yglesias’s words: “Whatever issues Harris faces based on her identity are issues she needs to navigate with her words and actions, regardless. I don’t think conjuring up a white male running mate accomplishes that.”

(At the time of publication, it was still my 140 mana propping her number up; if I sold them, she’d be back under 40%.)

Is this the biggest deal in the world? No. But wow, that’s a cheap price for objective-sounding publicity viewed by some major columnists (including some who’ve heard that prediction markets are good, but aren’t aware of caveats). And it underscores for me that conditional prediction markets should almost never be taken seriously, and indicates that only the most liquid markets in general should ever be cited.

The main effect on me, though, is that I’ve been addicted to Manifold since then, not as an oracle, but as a game. The sheer amount of silly arbitrage (aside from veepstakes, there’s a liquid market on whether Trump will be president on 1/1/26 that people had forgotten about, and it was 10 points higher than current markets on whether Trump will win the election) has kept the mana flowing and has kept me unserious about the prices.

Rationalists love our prediction markets. They have good features. They aren’t perfect. I like Zvi’s Prediction Markets: When Do They Work more since it gives a better overview, but for some strange reason the UI won’t let me vote for that this year. As prediction markets gain in prominence (yay!) we should keep our eyes on where they fall short and whether there’s anything that can be done to fix them.

I keep this in my back pocket in case anyone tries to argue that a thing’s high odds on Manifold is definitive. It’s a bit niche. It’s probably not super important.

Now, that being said:

At the time of this writing it’s 90% to get in the Best Of LessWrong collection, so obviously it’s an amazing post that’s very likely to be included and we should talk about it with the seriousness that deserves.

This post was certainly fun to write, and apparently fun to read as well, but I’m not very satisfied with it in retrospect:

I dunked a bit on people who didn’t deserve that tone; see the comments from Conflux and Nathan Young.

If I were writing it now, I’d also highlight that this form of cheap manipulation via self-fulfilling prophecy is a potentially fatal flaw with futarchy and even with fire-the-CEO markets.

It’s also notable as a real-life example of a spurious counterfactual being used to manipulate a decision! I of all people really should have noticed and mentioned that one.

I think the title was a bit overdone but the content was solid. Worth a read/think for prediction market people. We are perhaps a bit overly optimistic on prediction markets (eg this is a play money one) so yeah.

I think Yglesias is right to have couched his praise for the market in question but that is easy to forget.