Dissolving the “Is the Efficient Market Hypothesis Dead?” Question

(This talk was given at a public online event on Sunday July 12th. Alexei is responsible for the talk, David Lambert edited the transcript.

If you’re a curated author and interested in giving a 5-min talk, which will then be transcribed and edited, sign up here.)

Alexei Andreev: Recently, it’s been popular on LessWrong to claim that the EMH is dead. I want to talk about why hearing that annoys me, and then propose something that I think is better than EMH.

Quickly about me: I’m a co-founder of Temple Capital, one of the top five biggest cryptocurrency quant hedge funds. I spent the last three years developing quant strategies. Hence I have a bit of a practical experience. But I don’t study theory that much, so take this with a grain of salt.

There’s two things that annoy me when people say that EMH is dead.

First: what version of EMH are you talking about exactly? There’s a lot of formulations: weak form, semi-strong form, strong form, and, of course, the final ultimate mega form:

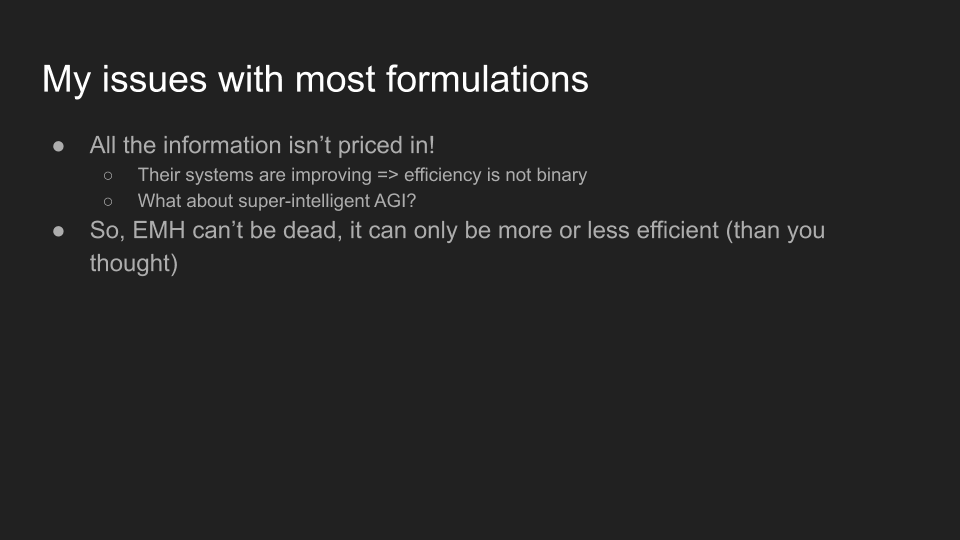

I have some issues with those formulations.

The main one is that they claim that “information is priced in”. I think it’s obvious that it’s not priced in, because who is pricing it in? It’s entities, agents, hedge funds and traders that are doing the work of pricing it in. And every day, they’re improving their systems, which means that yesterday they weren’t pricing in something that they’re pricing in today.

If you believe that they’re actually doing reasonable pricing, then they’re also doing reasonable improvements. The system is continuously getting more efficient. It’s not binary.

If you imagine a super intelligent AGI, and you give it just the most easily accessible, publicly available prices, I think it will still outperform most human traders.

EMH can’t really be dead. It can only be more or less efficient than you thought.

The second thing that annoys me when people say EMH is dead is: Why exactly do you think it is dead?

You have to read between the lines, and I think people are usually saying one of these two things.

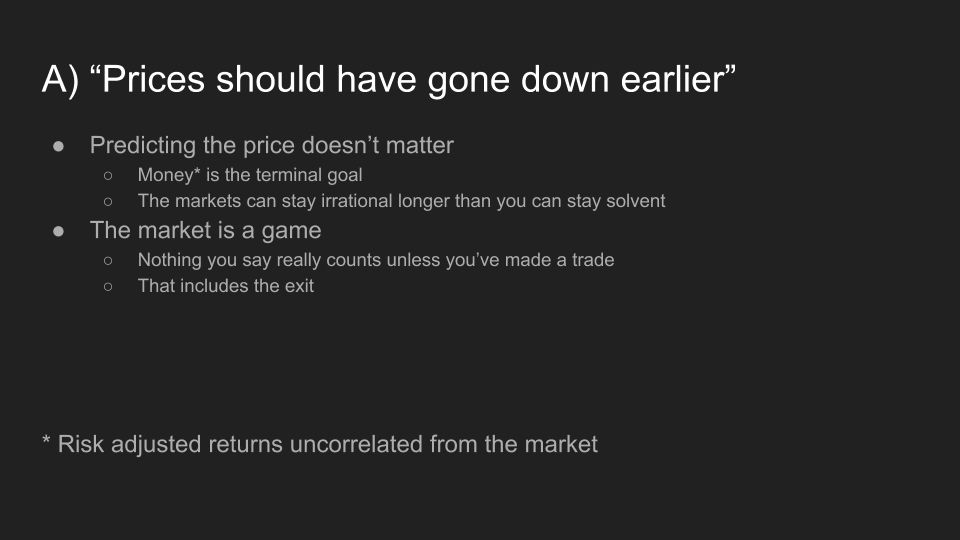

A: “Well, COVID-19 was obviously going to be bad. The prices should have gone down earlier, but they went down later. So obviously, the markets can’t be that efficient.”

B: “Well, I made a bet at some point on the market and I made money, therefore the market isn’t efficient.”

Let me address both of these points.

Point A: Actually predicting the prices doesn’t really matter. We’re trying to make money. That’s the terminal goal, predicting the price is just instrumental. You have to remember that the markets can stay irrational longer than you can stay solvent. You can correctly predict that the markets will go down eventually, but in the meantime you’ve entered your position, and they keep going up. You might get liquidated or you might just think that you were wrong and exit your position prematurely.

In my opinion, it’s more interesting and more accurate to think of the market as a game. You make trades in the same way that people playing games make plays. You shouldn’t talk about what the market should have done unless you have made a trade and participated in the game. And that includes exiting your trade. Please don’t talk about how you have bought some stock at a very low price until you’ve actually sold it.

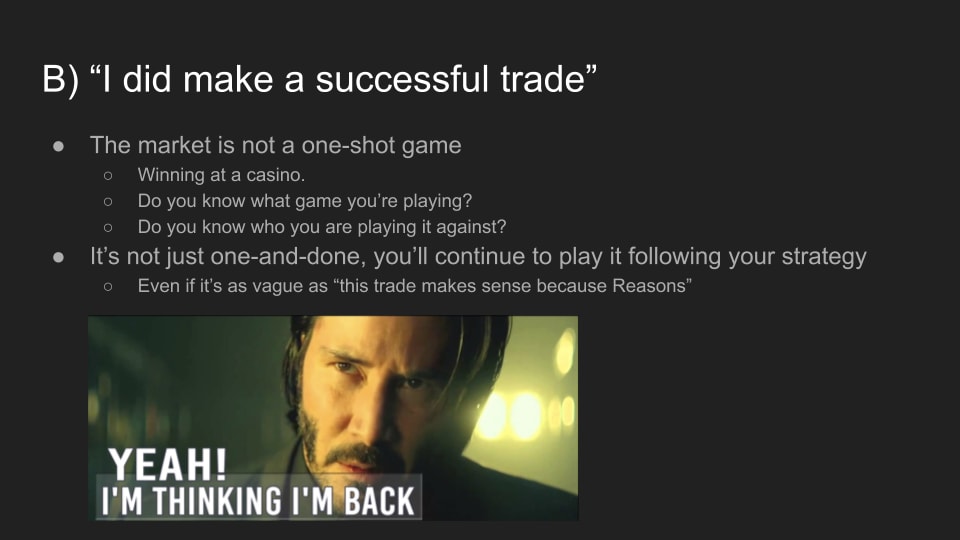

Point B: “Oh, I made a successful trade. Or maybe two, maybe three.” Well, the market is not a one shot game. It’s like if you go to a casino and you bet everything on red and double your money. You can’t really say, “Well, I beat the casino.”

We know this is kind of silly, because we know that the game is unwinnable. But why does it make sense to say that you beat the market? Do you really know what game you’re playing? Do you know who you’re playing it against? I think you have to realize that it’s not just one and done.

If you’ve made a bet, you’re kind of then bound to follow the strategy that you set up for yourself. Suppose you say “It makes sense to me to make this bet.” Well, the next time it makes sense, you’re going to make another bet. And the next, and so on.

You can’t quit this game once you’ve started.

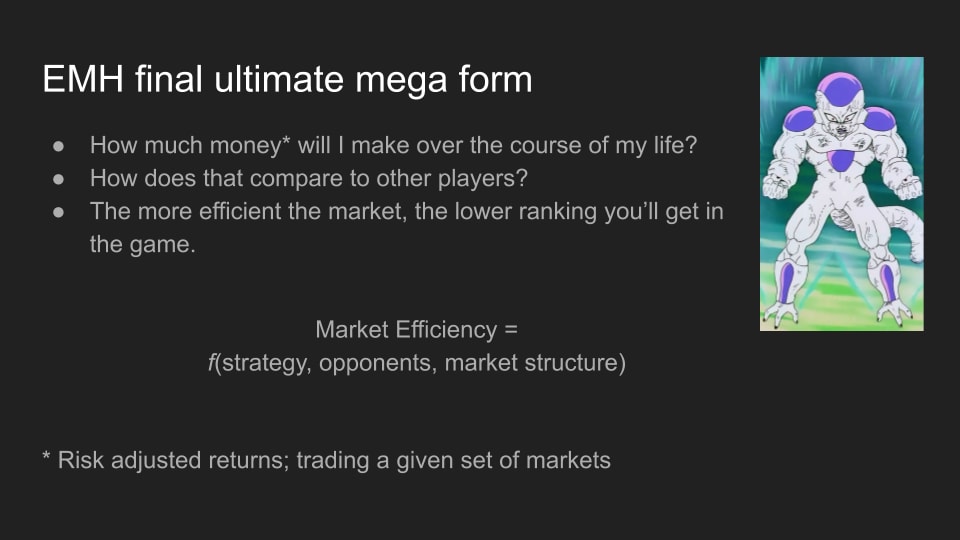

So my proposal for the final ultimate mega form of EMH is to really ask the question: how much money will I make over the course of my life? How does that compare to the other players participating in the markets?

The more efficient the market is relative to you, the lower your ranking will be in this game. I think of the market efficiency as a function of the strategy that you’re running against your opponents, and the market structure (or the game structure).

Questions

David Manheim: You talked about how market participants update their models and improve over time, so obviously it’s kind of a dynamic game. Now it seems like there’s a value of information component here. There’s a cost to updating, and it’s unclear until after somebody has paid for information whether the information or the updates are valuable. And then there’s some heterogeneity between agents about which information they have access to and how difficult it is for them to update.

Do you think that plays into the market being less predictable? Or into there being gains to be made in the market if you can identify where you have a marginal benefit and receive new or updated information?

Alexei Andreev:

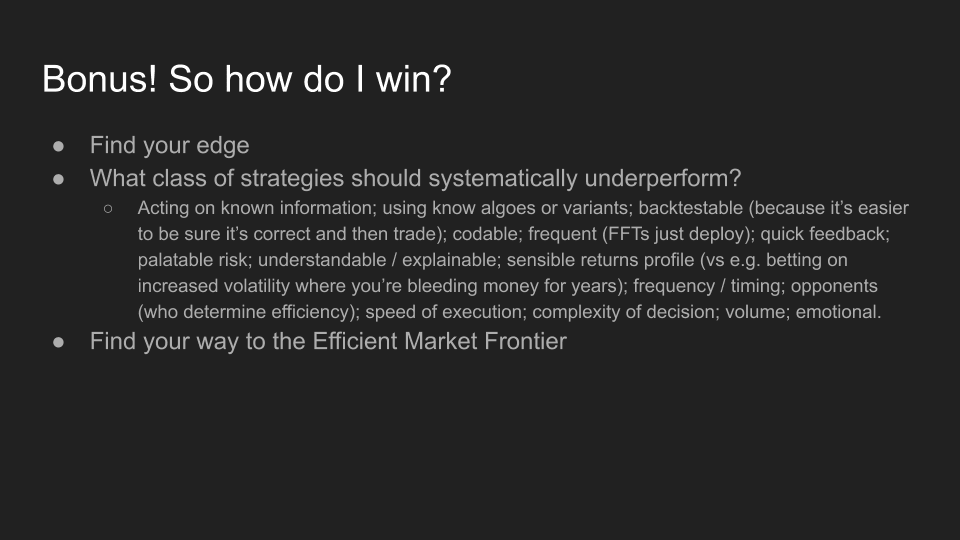

Yes. Actually, I made a bonus slide that I think will help here. This is not quite an answer, but I think a question related to what you’re asking is “How do I win?” And I think you win by finding that edge, on what I would call an efficient market frontier.

There is a large number of variables that go into a good strategy. And so, one way to look at it is, is to ask what makes a bad strategy? If you’re acting on information that everybody knows, it is probably a bad strategy. If you’re using algorithms that other people are using, it’s probably a bad strategy. If you’re doing a manual trading that can be written in code and automated, it’s probably a bad strategy.

This slide covers a bunch of these things.

I think an interesting thing about people betting on COVID is that it’s actually the opposite of most of what is listed, because you’re using human intuition. Nobody is really running coded algorithms that are detecting the beginning of a pandemic and shorting the market.

For most hedge funds, it was probably a very manual decision that took a few days, and they were moving a lot of money. And that’s also one of the functions here: how much money are you trading? It’s much easier to make $1000 than $10 billion.

---

Oliver Habryka: Over the last few months, I’ve been trying really hard to understand what market prices mean. I mostly updated it’s just really hard to understand what they mean, and so it feels very confusing for me for the EMH. Because I’m like, “Oh. How many other people don’t really understand what market prices mean?” A bunch of the people who I trust the most were really confused what market prices mean, and now everyone is like, “Yeah, stock prices are obviously up because real interest rates are down.” What’s going on here? If you told me that we produced fewer things, I would have expected stock prices to go down, not up! That doesn’t make any sense.

So I’m looking into this and trying to understand what is happening. I do expect some people have a much better grasp on this.

I’m trying to get a sense of how much I should believe that there is a territory to be traded on. What I am actually predicting when I’m trying to predict the market. Am I just trying to predict the actions of everyone else? Sure, to some degree. But that feels to me like something that makes all this weirdly anti-inductive and I don’t know how to handle it.

I’m sure you can bypass all that by just being like, “Run a bunch of automated, back-tested strategies and see what they look like”. But it still feels to me like it bypasses an important question.

I don’t really know whether there’s a question here. But if you have any pointers about how I can understand this, I would be deeply grateful.

Alexei Andreev: Yeah. I think it helped me personally to trade in crypto because I know there’s no logical reason why the price of bitcoin should be $10,000 instead of $1, other than that being the point where supply equals demand. But the price doesn’t really mean anything.

It’s more like, “if you can predict what other agents think is a fair price, then you can predict when they’ll buy from you or sell to you, which helps you play the game”. But I think it’s purely instrumental.

Ben Pace: Overall, to me, that is quite an update, and I’m doing some re-conceptualizing. It’s not so much that the EMH is false, but in a bunch of situations it seems less epistemically helpful when I’m trying to figure out the state of things. I would naively expect to track the state of reality. But this requires doing a very different sort of calculation. I’m curious about your opinions on how easy it is to understand what the markets are saying.

Alexei Andreev: Yeah. I think it’s hard most of the time. But if you do understand then you can make money.

---

Satvik Beri: I would like to make a statement, correcting a few minor inaccuracies. Just nitpicking.

I work with Alexei. He’s heard me say all these things before. Oli, to your point, I think in some domains, there are forces that pull prices towards certain things, and in some domains there aren’t. Prices can diverge quite a bit in the short term, but tend to converge in the long term towards those things. For example, prices are not completely unrelated to long term expected corporate profits, even if they can diverge quite a bit.

Another point: Alexei said that a highly efficient market is one where you expect your rank to be low. But I think it’s more accurate to say that a highly efficient market is one where you expect your rank to be average in the game and it’s very hard to break out of the average. It’s even hard to underperform intentionally if the market is efficient—because you could always do the opposite.

---

Ozzie Gooen: I think I’ve been quite frustrated by people talking about the efficient market hypothesis as it’s like a binary thing. That itself seems quite stupid. But the fact that COVID alone should create a massive update also seems quite wrong.

Alexei, in the final slide, you had an equation of market efficiency: f(strategy, opponents, market structure).

Now it does seem to me like at least some hedge funds and other groups are making money, repeatedly, in the market. And my impression is that a lot of them are making financial cost-effectiveness decisions on whether they should invest money in new researchers, and parts of the market where they expect to see some return. It does seem like it would be possible here to make theoretical models.

So I would have expected to see a bunch of econ papers trying to model the market this way. That is: actors paying costs, in order to obtain knowledge and do research. Maybe modelled using agent-based modeling, or whatnot? Are there good examples of papers like that, or other functions like your f(strategy, opponents, market structure)?

Alexei Andreev: That’s a great question. It’s not something I would know. Because like I said, I am a trader, and haven’t worked in that kind of academic research. It’s also tricky to do that kind of research in this field, because to the extent it helps you make money, nobody will really publish it. (They’ll just go and make money instead). Most of the stuff you find is either very theoretical or just flat out wrong.

Regarding Ozzie’s point above about markets where agents can pay to acquire costly information; this is the famous Grossman-Stiglitz paradox (1980), and indeed the paper concludes that informationally efficient markets are impossible in this setting.

https://en.wikipedia.org/wiki/Grossman-Stiglitz_Paradox

I wanted to write a post on this topic for a while, but couldn’t find the time. I’m glad I got to do the talk instead, since that helped me with narrowing down the scope.

I have more thoughts I can type up, if people are interested.

I quite enjoyed this and found it useful. Would love more thoughts.

Definitely interested, especially if there are more details you can give about the options bets you mentioned in this comment.

I’m only vaguely informed about options with no experience buying them, so I likely need to learn more before I can ask useful questions about this, but I don’t want to miss the opportunity to say I’d definitely be interested in any thoughts you might be considering posting, since I’m interested in this type of general bet on AI progress.

Anyway, I know you can’t give investment advice and don’t expect you to teach me how options work, so I guess I’m just hoping for details that help figure out if I’m thinking about this correctly, specifically with respect to using options to bet on certain short AI timeline scenarios.

(For concreteness, my general understanding is something like: say I decide the bet to make is on GOOG stock. So I set aside $X per month to buy “long call” options on GOOG as you indicate in this comment. And I should be prepared to typically lose all of that $X each month, unless the bet pays off.)