There were a bunch of discussions recently related to issues surrounding Y-Combinator, related as usual to their annual demo day. It seemed worth splitting them off into a post.

Bidders at Auction Mostly Think Prices Are Too High

YC is in session, so all the usual talk is back.

Paul Graham: As happens every single YC batch, investors complain that the valuations are too high, and the startups raise anyway.

Kush: Is there any specific reason why you think this happens?

Paul Graham: Some investors just cannot grasp the implications of the fact that all the returns are concentrated in the big wins. The top tier investors get it though; you’ll rarely lose one of them over price.

Amal Dorai: Isn’t the dynamic range of YC valuations narrower than the companies themselves? We see pretty much a 2x range that they’re raising in, but >10x variance in current traction. The high flyers are fine but those riskier companies still finding their footing are behind the 8 ball.

Paul Graham: The variation in valuations is much smaller than the variation in quality. That’s what determines risk, not their current traction. If current traction were a perfect or even good predictor, investing would be trivially easy.

David Tran: “You’ve found the market price when buyers complain but still pay”

Dan Grey: What I’ve seen investors saying is that they would rather wait a year and then invest in the next round – which happens at a similar price but with much more proof. If the initial round is not offering the right level of upside for the risk, why should investors jump in?

Paul Graham: That was an amusingly novel variant. I only saw one investor say that. The reason it’s a dumb strategy is that choosing companies whose valuation hasn’t increased a year later selects for bad ones.

This model tells me that the lower valuation, less exciting companies in YC are likely overvalued, and the higher valuation, more exciting companies in YC are highly undervalued.

I see two distinct dynamics here, the one Graham and Dorai raise, and Tran’s.

Tran’s is the core reason investors complain prices are too high. Of course most investors think the YC prices are too high. There are tons of investors chasing not that many YC companies with not that much space in their rounds. YC companies have many advantages over non-YC companies, including all three of:

Selection effects (I don’t think there are zero bogus AI companies in the round, but YC is excellent at picking good founding teams and promising companies).

Endorsement effects (YC pedigree is a strong signal and coordination point, everything will be easier with the name attached).

Enrichment effects (YC gives you an amazing network and toolkit, and teaches you a ton, and gives you motivation and focus).

On top of that, there is the compression of valuations effect.

YC companies are wisely advised, the internet reports, to raise floor prices on rounds, because it saves you a lot in terms of ownership and with the YC name you can expect to raise the funds anyway. So the relatively non-exciting companies charge a lot, as they should. Why would you sell more equity for less money when you can sell less equity for more money?

You Would Pay For The Ability To Charge More

Paul Graham points out that this whole dynamic makes YC valuable, and the witnesses are highly credible.

Would-be founders: When later stage investors complain, as they always do, that the Demo Day valuations of YC companies are too high, what they’re saying is that doing YC will enable you to raise money with less dilution.

This is a valuable claim for YC to be able to make, but it’s even better when it’s made for YC by people who clearly don’t mean it as a compliment.

It does not matter, from the startup’s perspective, how much of their increased value comes from endorsement versus enrichment. It does matter to them to what extent it is selection.

I will also note that the existence of YC lowers the valuation of every company that is not in YC. You know that if they could have done YC, they probably would have, so you are fighting against highly adverse selection. All the more reason to do YC, then.

The Best Deals Come With the Best Prices

The most exciting companies in YC charge a lot as well, but it looks like they don’t charge all that much more. There is as I understand it a convention in the space about what valuations are ‘supposed to be.’ You can vary within the range, but once the founders are raising at an unusually high valuation right out of the gate, the price matters a lot less because they are giving over much less of the company. So rather than raise more money in exchange for less of the company, focus often shifts to gaining allies, setting up a path and telling the right story.

In particular, considerations of avoiding possible down rounds, and choosing the right strategic VC partners, seem to dominate price considerations at the high end.

You rarely lose a top VC over price because there is strong desire on both sides to not let this stop the deal. The startup gets better VC flow to help it down the line, and the top VCs get the better deal flow that provides most of their alpha.

From the startup’s perspective, this is epic highway robbery, using the conventions of VCs to buy equity for far less than it is worth, but given the situation they are well advised to pay up.

If you are a top VC, this is amazing. You keep putting out a quality product, and YC will give you great deal flow, shining giant lights over great opportunities that don’t use their full pricing power.

If you are not a top VC, this is a big problem. Adverse selection is happening now, not only in the growth of valuations later. If you could invest in a broad portfolio of companies at YC that look good to you, or even YC companies overall, that would be fine. The problem is you cannot do that, so you are looking at companies with 10% the hit it big prospects of other companies (that won’t answer your emails because you suck and they can do better) but 50% of the valuation, and saying the price is too high.

Jeff Weinstein: YC startups that would have raised at $8M cap in 2017-2020 are today raising at $20M cap.

In part this is due to the larger YC investment and MFN, but it also feels like these companies are being given bad advice and remain in denial that we’re not in 2021 anymore.

This is fine if you execute absolutely flawlessly, find PMF, and raise enough to give you years of runway, but more often than not it puts startups in a tricky spot in 12 months, when they are valued on multiple instead of story.

Given these founders are raising at uninvestable prices around demo day, more and more often we are passing due to price and revisiting in 12 months!

Amjad Masad (CEO Replit): This is just market dynamics — nothing irrational on the part of founders. The alpha is simply dissipating (you are not entitled to alpha).

Those who will continue generating returns are the great pickers who can get great ownership % and the ones investing pre-seed (and pre YC).

My only quarrel with Masad here is that one must be careful not to confuse great picker with good deal flow. There is definitely no reason VCs should be entitled to alpha, or the majority of YC investments should even be good deals.

For startups, a consequence of this dynamic is that most startups get huge value out of YC via raised evaluations and reputation, but the very top startups do not. They were already sending out strong enough signal that they were going to write their own ticket when raising money and not charge the market clearing price, so raising the market clearing price does little.

Should those top companies do YC anyway, despite the cost in equity? It is less obvious and likely differs case by case, especially since you can never be sure early on if you are or will remain one of these companies, and YC can help turn you into one. If I was in a life position were I could do YC and was founding a company that fit, then no matter how good things looked, I would definitely apply intending to accept if they said yes. If I gave up a little value, I am doing so well I don’t much care.

Raise Early, Raise Often, Raise Everywhere

Kyle Harrison offers what seems like good advice, most of which is standard. Start raising with more than a year of runway because it takes variable time that can get long and now more than ever you cannot count on VCs to actually deliver. Cast a wide net and talk to many VCs, but be straight about who you are and what kind of fit you need so time isn’t wasted on both ends.

He suggests writing a memo that articulates things, rather than pure reliance on a deck. That certainly seems like a superior equilibrium.

Good VCs Get Their Money Back Surprisingly Often

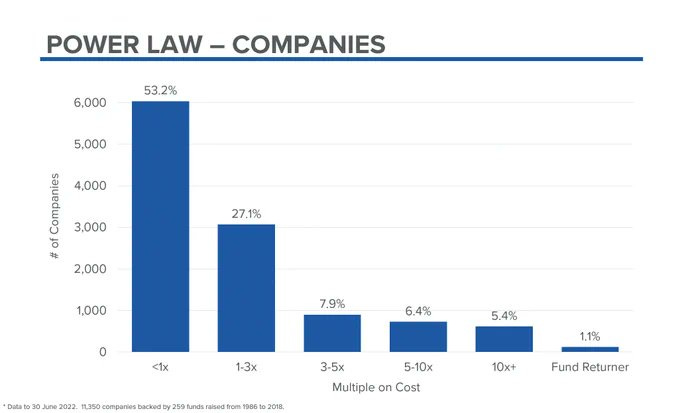

Paul Graham sees a different takeaway than I do on this next point.

Paul Graham: David Clark of VenCap analyzed the returns from 11,350 startups backed by 259 funds from 1986 to 2018. About half these investments lost money, but 121 (1.1%) returned the entire amount of the fund that invested in them.

Two of their top ten investments were founded after 2010. Both are YC companies. That’s what draws later-stage investors to YC. The valuations may be high, but it’s where the really good startups are, and that’s what matters most for returns.

David Clark: Top 10 fund returners by multiple of cost are as follows: 10. Coinbase 9. Slack 8. Portal Software 7. Facebook 6. Avanex 5. Google 4. Ariba 3. Yahoo 2. Brocade 1. DoorDash Multiples range from 140x to over 800x

Instead, I had Yuri’s reaction.

Yuri Sagalov: I’m actually surprised only ~50% of the investments returned <1x. I would have thought that number would be higher.

Paul Graham: Me too. But we live in the early stage.

If you can simultaneously get your money back 46.8% of the time, and also have this distribution of profits, that is a fantastic business. This is a 36.8% return even if you discard the Fund Returners entirely and mark everyone else to the extreme low end of their ranges. Yes, the FRs are important, and if we have 259 funds making ~12k investments they start on average at ~50x, but you don’t actually need them if you only fully miss half the time. As Paul notes these will be later investments, but also not that late.

If You Want it Done Right

Gusaf Alstomer (of YC) notes that using a designer on your pitch deck never works.

Gusaf Alstomer: Pitch-deck advice: I don’t think I have ever seen a fundraising deck getting better by using a designer to design it. The same goes for using fancy tools like Figma, Keynote,

http://Pitch.com, or Canva. At @ycombinator we recommend people to use Google Slides and keep it simple. The two mistakes founders make are believing that the creative capabilities of the tools make a better deck. The second mistake is believing that the design is important.

The most creative people operate under constraints. And the most powerful tools are your words and storytelling. Clear communication and relatable storytelling allow a listener to put themselves in the seat of the person having the problem you are solving. The best way to visualize this is with real photos of real people having these problems.

The best fundraising decks have this structure:

1) Headline that concludes the point you are making

2) 3-4 bullets with evidence towards the point you are making

3) Repeat until you’ve covered all conclusions

4) Wrap this in a storytelling narrative – tie the slides together with a story

5) Whenever possible, only use real photos and if you use screenshots, zoom in on the thing that tells the story

The exception to the “don’t hire a designer rule” is when the founder themselves is a designer. They know what is important about this business – another person will never know this.

This very much matches my experience as well. Designers have a very different skill set and are aiming at a different target. They don’t understand what matters, and what matters will often change quickly or as you shift contexts, and you will want to edit on the fly. The deck also needs to be congruent with you and match your voice. Yes it is good if your deck looks nice but ultimately that does not much matter.

There is an important general point here. When there is a primary expertise that matters most, you will often see people making horrible errors in secondary areas, because the winning play is to focus on what matters. I wonder if AI will alter this.

You’ll Need the Time to Do That

A common productivity theme is that by default people do a lot of grunt work that eats up a lot of their time. Another is that taking care of the fundamentals and getting your house in order gives you a big leg up.

If your time and efforts are valuable, and especially if you are a founder and have increasing returns to effectiveness deployed, perhaps someone should help with that?

Avi: I would pay so much money for a single service that completely handled my basic needs so I could focus

* laundry

* 3x/day meal prep

* personal trainer

* cleaner

* therapist turn my house into a monastery.

This should be VC value add. Founders should treat themselves as athletes

Mason: Don’t say it

Don’t say it

Mason don’t

Aaaaaaaagh IT’S A WIFE YOU WANT A WIFE

Avi (distinct reply to his OP but this order is more logical and also funnier): Funny thing is if I tweeted this saying I want a wife to do this for me I’d also get flamed. I feel that if you raise funding, part of it should *temporarily* go to removing distraction. This includes healthy meal prep, sleep tracking, etc. I know the tweet comes off a bit inane, but I’m a single 20 year old with no intention of getting into a relationship. I live and breathe my work. Twitter is my only vice.

Misha Gurevich (responding to OP): I think too many people watched Batman as kids and have an idea of “monasteries” as training centers for turning you into a badass instead of fundamentally boring places where you do manual labor in poverty and pray.

A lot of people seem to think if they had a butler he would be the Albert to their Batman but really they want a Jeeves to their Wooster.

“Jeeves is a valet, not a butler; that is, he is responsible for serving an individual, whereas a butler is responsible for a household and manages other servants. On rare occasions he does fill in for someone else’s butler. According to Bertie Wooster, he ‘can buttle with the best of them.’”

Credits You Will Need More of Are Essentially Money

Yuri Sagalov: Founders, if you’re in the fortunate position to have AWS/etc credits, don’t treat them as “free money.” Instead, treat it as extra cash on your balance sheet that you can only use for one purpose, and count your AWS usage as part of your burn. Don’t wait until they run out.

James Hu: This is the same way to think about credit card points and miles. It’s cash, and just as good as cash for anyone who travel, and should be treated as such.

Exactly. If you have credit somewhere and will inevitably spend it and then keep spending, that credit is functionally no different from cash. Spending it is no different from spending cash. The same goes for any other asset that can be used in place of cash. If it would otherwise go to waste, then that is different, otherwise its value is equal to the opportunity cost. Which is usually damn close to $1 per dollar.

Get Your App Out There Quick

Apple Hub: The App Store and iOS are now officially designated as gatekeepers in the EU and will need to comply with the Digital Markets Act (DMA) This means Apple will be required to allow users to downloads apps from the internet and third-party app stores.

Do you agree with this regulation?

Emmett Shear: Woah this is huge news if it gets enforced. Would be the best thing for the tech ecosystem in a long time…if the USA doesn’t follow suit will actually significantly advantage European startups! Or at least startups deploying in EU first.

There was no poll, which I am guessing was the right choice by Apple Hub.

I would not be in the habit of regulating such matters, but if I was, this would be a good choice of regulation. It does seem first-level helpful.

What does this do for startups? It means you can get your app to Europe’s iPhone users without the app store. If you can find them without the app store. If they are willing to side load. Which will be rare. People do not like to sideload even on Android, where it is supported and you have people opting into that ecosystem.

My prediction is that this does not end up having that much practical impact.

No, Quicker Than That

Bri Kimmel: This is the first YC Demo Day in a very long time where the majority of B2B companies had paying customers, recurring revenue, and large contracts with companies way too big to work with a small startup.

Garry Tan (President of YC): 75% of the companies presenting today started with no revenue on day one of YC. 81% had never raised a dime. During the past 3 months, we pushed the startups hard to build meaningful software and sell it. This is the speed up that I have only ever really seen YC do for founders.

Joe Benjamin: Why do you think so many founders are slow to go out and sell when starting out?

Garry Tan: Fear of failure.

How easy it is to forget that selection effects and network effects and other affordances are in play.

If you are in YC, you have been selected by Garry Tan and others based in large part on them thinking you will soon be able to go out and sell, then they are giving you lessons on how to do that, network connections and other resources to help you do that, helping sculpt your pitches and targets and such, and also giving you the ‘I’m in YC’ foot in the door that I presume helps with large companies. You have the tools to make sacrifices in order to do the selling, in turn in order to go faster and get better valuations and also learn faster. And of course they exert massive social pressure in the other direction.

If you are not in YC, you are in a very different situation all around. It is very possible to be attempting to sell too much too quickly, before you are ready.

Failure can also be not only damaging but cascading. Games that come out and try to get revenue too early and fail to sell are marked as failures, I have had this happen to me and watched it happen elsewhere – the game improved later, the algorithms and fans have moved on, it is too late. A focus on revenue before it is too early can also waste your time, tell the wrong story that breaks your ability to continue or raise, burn your best leads and plays before you are ready, or otherwise devastate.

So no, I do not think this decision is that easy, even if what are otherwise the best startups would be better served selling more and selling faster. I have had multiple experiences with the opposite mistake.

All The Startups Are Now AI Startups

Meanwhile, Paul Graham continues to notice that YC is now all about AI.

Paul Graham: I haven’t been more optimistic about YC since I retired in 2014. Garry has been doing a great job, and the current batch is a particularly good one.

The AI boom will be very good for YC. It will mean a lot more startups, and the kind of founders who win at it are the kind that YC specializes in.

YC has already been transformed by the AI boom. I’d guess more than half the founders in the current batch are working on AI startups. It’s like an ongoing AI symposium with over 200 participants.

I actually buy this. A YC-style team and approach are unusually well suited to this moment, YC’s infrastructure will be a big help, and YC will largely have its pick of founders. What a great time to be YC.

I would once again however double down that there are doubtless quite a few bogus AI companies involved. Nothing becomes this ubiquitous, this all-consuming, this hyped, without bogosity. Failure to spot them, however, does not automatically mean you are the sucker. It is a hits-based system, so what if some of them aren’t real? What matters is the deal flow giving you access to the best stuff, not avoiding false positives.

So, what are all these non-bogus companies up to?

Aaron Levie: All the enterprise AI startups going after verticals have the right idea. Pick a market, deeply understand the workflows, build simple software to model the workflows, and use AI to augment the human judgment involved. Huge opportunity in 1,000’s of categories.

Paul Graham: This is the median startup in the current YC batch.

I have certainly seen worse plans. Enough to fill out a demo day. I would doubt that there are thousands of such categories offering great opportunity.

Man With Moat Unconcerned With Non-Flying Creatures

What happens if someone copies you? Don’t worry about it, says Paul.

Paul Graham: When people copy you, the best strategy is usually to ignore them. People who copy you are (a) unoriginal and (b) opportunists, and those are both strong predictors of failure. If you wait them out, they’ll eventually drop away.

Joel Fraunsic: “I’ve been imitated so well I’ve heard people copy my mistakes.” ― Jimi Hendrix

Paul Graham: This happened with both Viaweb and Y Combinator.

When people attempt to make exact copies on various levels, yes they usually fail, but often they also don’t, and if there are lots of imitators most of them failing does not mean that you can safely ignore the phenomenon. The advice to ignore them goes hand in hand with working actually super hard to ensure that one can safely ignore them, by being the best like no one ever was and continuously improving and having strong reputational and network effects. In which case, sure, bring it on.

If they are not exactly copying you, rather taking you as reason to compete, that is in a sense great news about your situation absent the competition, but it definitely should worry you, especially if the competition is well-resourced. Noticing one example…

Danny Alberson (CEO Agentive,YC ’23): I recently met with a VC firm twice, showed a product demo, and answered countless questions about our strategy. Only to find out from someone else they were already invested in a direct competitor.

Paul Graham: I just sent you an email. This should go in the investor database.

Danny Alberson: Absolutely. Thanks for following up.

Absolutely. Thanks for following up.: Please consider open sourcing it!

Li Ang: An open source database is very much needed.

Ronak Shah (other reply): This happened to me too. Not only the calls but they kept asking for my financial model so they could see my pricing / how I won big logos. They hid the fact that they invested in my competitor.

[several other replies noted similar behavior, especially related to Web3/crypto]

Garry Tan (QTing Alberson): Warning to investors: there are consequences to this kind of behavior. I will personally make sure of it.

Austen Allred: I love YC.

Ryan Peterson: YC invests in competitors constantly though.

Paul Graham: This isn’t a case of investing in a competitor. It’s a case of pretending to be interested in a company in order to pump it for information.

The Investor Database Is a Killer App

There are a lot of services you get from YC. Given how multiplicative everything is when it comes to startups, it does not take much to get a big payoff. Purely raising your ambition alone is great, many other seemingly simple principles are great.

The payoff that impresses me most is the reputation, followed by the network. The most underrated is likely the broadly construed investor database, where you get intel on all the venture capitalists.

It is vastly different dealing with people whose actions have been and will be recorded into a central database. The VC knows that you will report back. You get to use the previous reports to know which VCs will treat you well, offer which resources, use which styles of negotiations, respond well to various approaches, and so forth. If the information is accurate, the ultimate impact on ability to raise money, from the right people, under the right conditions at the best price, seems colossal.

While I understand why one would want to retain this competitive advantage, it would be wonderful if this information could be disseminated to everyone. Behavior would improve, those who treat investors well would get rewarded, and outsiders in particular would have a much better shot at being founders. Even if I’m not that excited to accelerate the ability to create AI startups right now, this has to be the right thing to do.

Would it be expensive to YC to give this up? My instincts say that it would not be. It would be amazing advertising, it would fuel the ecosystem and it would demonstrate value. There are enough additional advantages to YC that I predict most founders would not change their decision whether to participate. YC is not charging a market clearing price.

I recently met several YC founders and OpenAI enterprise clients — a salient theme was the use of LLMs to ease the crushing burden of various forms of regulatory compliance.

Isn’t that, like, the very definition of an auction? People offer different amounts of money, the one who offers most buys the thing, everyone else offered less… which means that they consider the final price too high.

Indeed! The primary reason to have an auction rather than a fixed-price first-come-first-served offer is to FIND the buyer who values it highest. This selection effect guarantees the price will be higher than others are willing to pay.

I think the main beneficiaries of being able to sideload apps will be incumbents, not startups. Big companies like Spotify, Netflix, and Tinder will offer users discounts if they sideload because it will spare them the 30% Apple tax.

I’m not sure how much you can say this based on count of deals, unless you know if there are differences in deal size between the different ranges.